2025

The State of B2B Payments

How finance leaders are navigating growth, risk, and the future of digital payments.

Download Report

The State of B2B Payments

2025

Explore insights from 746 finance leaders on how they're managing cash flow, fighting fraud, and scaling smarter payment systems.

What's changing in business payments?

SMBs say digital B2B payments are essential to operations and protect against fraud.

25%

of SMBs experienced fraudulent fund transfers in the last 12 months

#1

Paper checks are

still the top target for payments fraud

still the top target for payments fraud

83%

of businesses say digital payment platforms are essential to their operations

What's in the report

Chapter 01

Digital payment adoption

SMBs are embracing digital payments platforms for their speed, efficiency, and fraud protection.

Chapter 02

Tech stack deep dive

88% of SMBs say a digital payments platform is important to the ability to scale.

Chapter 03

Cash flow under pressure

Half experienced cashflow concerns in the past 12 months. One third expect future challenges.

Chapter 04

Fraud and security risks

Payments fraud is the top financial concern, but many lack confidence in their protections.

Chapter 05

Looking ahead

As SMBs scale, security, speed, and tracking will be top priorities over the next three years.

Digital payments platforms are essential to SMB growth

"The data reveals a fundamental shift in how SMBs view B2B payments. It's no longer just about moving money—it's about building resilience, preventing fraud, and enabling growth. Businesses that embrace digital payments platforms are positioning themselves not just to survive, but to thrive in an increasingly complex financial landscape. The message is clear: modernize your payment operations or risk being left behind."

Mary Kay Bowman

EVP, GM of Payments and Financial Services

BILL

EVP, GM of Payments and Financial Services

BILL

Cash flow concerns

Is cash flow a significant concern?

Half of SMBs had cash flow concerns in the past 12 months, and one third expect to have cash flow concerns in the coming year.

51%

had cash flow concerns in the last 12 months

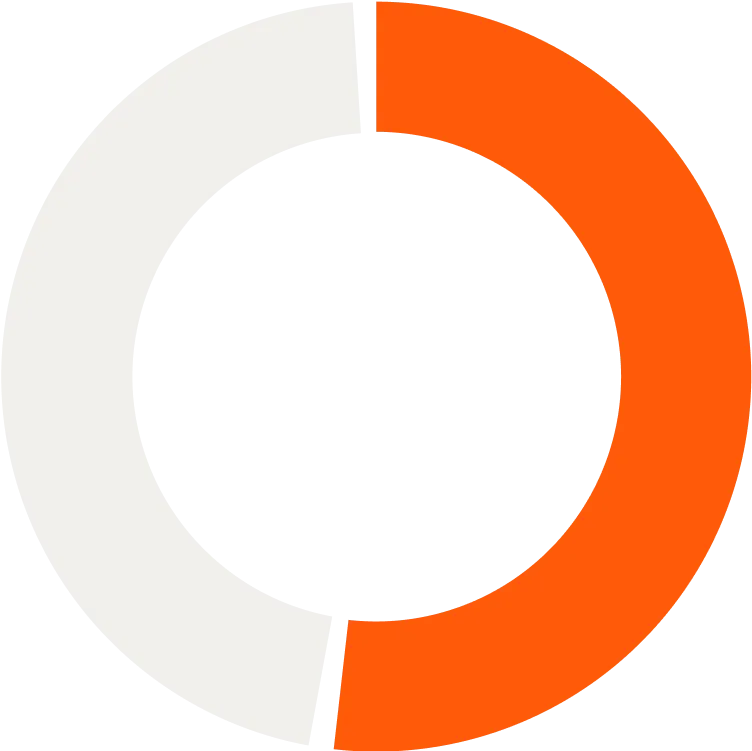

Fraud and security risks

Are security measures for B2B payments good enough?

Despite widely implemented security measures against B2B payments fraud, half of SMBs are not very confident in the efficacy of the measures they've taken.

44%

Very confident

55%

Not very confident

About the survey

Bill’s 2025 State of B2B Payments survey, conducted by Logica Research, was fielded in March 2025. We surveyed 746 SMB executives in the U.S. who have significant or final decision-making authority over their company’s financial software.

Number of Employees

% of Respondents

100+

35%

10-99

35%

Less than 10

30%

Download the full report

Get the full report to learn how other finance leaders are approaching 2025’s challenges with confidence.

Oops! Something went wrong while submitting the form.