Your financial reporting tells many stories. The answers to questions about profitability, growth, debt, and more can all be found in financial statements and transaction histories.

But to have these resources ready at your fingertips, you need to put in the work to maintain them.

An example of this is your accounts payable ledger—the key to understanding the when, where, and how much is being processed in your accounts payable cycle.

And to have the ledger ready for review, you need to create accounts payable journal entries.

What is an accounts payable journal entry?

Accounts payable journal entries are made in an accounts payable ledger whenever a transaction relates to a purchase from a supplier made on credit.

The two most common types of accounts payable journal entries are receiving an invoice and making an invoice payment.

If you’re wondering whether an accounts payable journal should be entered, ask yourself whether the accounts payable balance is changing.

If the balance is going up or down, you need to create a journal entry to reflect that in your books.

What’s included in an accounts payable journal entry?

An accounts payable journal entry is made up of the following:

- Date

- Description

- Amounts

Date and description are straightforward.

The date is when the transaction took place and the description is based on the information you want to capture—usually the invoice number, who it’s from, and a short summary of what was purchased or why the entry is being made.

The amount is broken up into two components: debits and credits.

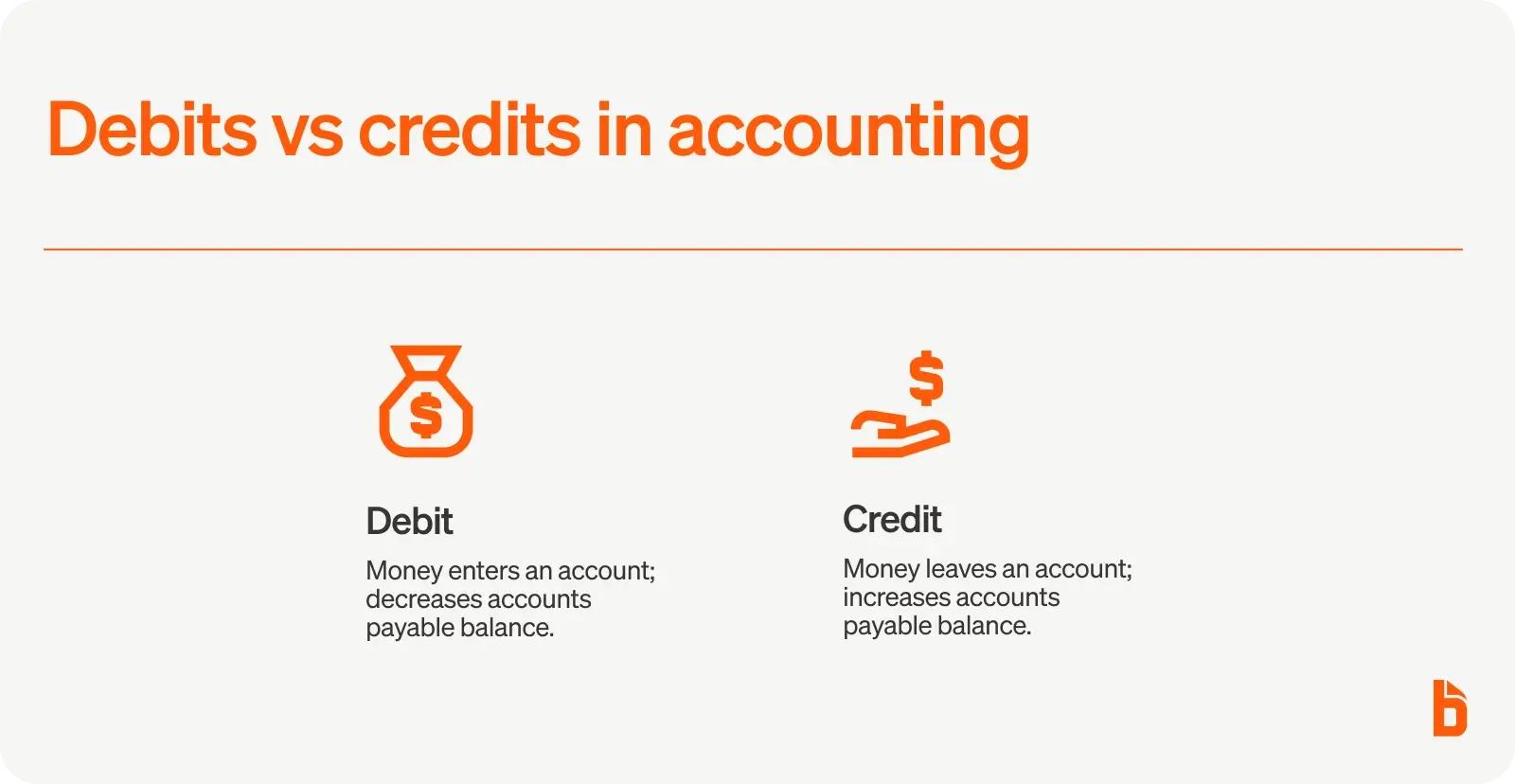

What are debits and credits in accounting?

In double-entry accounting, every transaction is made up of debits and credits.

When an account is credited, money is “coming from” or “leaving” the account while debits mean money is “entering” the account.

For every accounts payable journal entry, your accounts payable account will be either credited or debited.

When it’s credited, the balance increases, and when it’s debited, the balance decreases.

Debits and credits must be equal on every transaction and on the account as a whole.

If there’s a discrepancy between the two, some money has been unaccounted for.

When do you make an accounts payable journal entry?

An accounts payable journal entry is made any time your accounts payable balance changes.

The most common examples of this are when an invoice is received (balance increases) and when an invoice is paid (balance decreases).

You also need to create what are called adjusting entries in the case of an invoice being changed or voided.

For example, if you’ve already logged an invoice for $1,000 but the supplier changed the billing amount to $800, you create an entry adjusting for the $200 difference rather than edit an existing transaction.

Why create an adjusting entry rather than edit or delete a previous entry?

The answer is completeness and accuracy.

If someone comes across an unpaid invoice, they can review the ledger to check if it was voided or adjusted before making a payment.

Accounts payable journal entry examples

To help illustrate how accounts payable journal entries work, let’s look at five examples of when you’d make a journal entry and what it would look like.

Your accounts may differ from the accounts we use in these examples.

Refer to your chart of accounts to confirm what account you should use when you’re making an accounts payable journal entry.

Entering a received invoice

At the start of April, you submit an order to top up your inventory.

Altogether, you’re buying $10,000 worth of products.

Once the invoice is received, it’s time to create the journal entry.

The date is the date of the order as noted on the invoice, April 1st.

For the description, note the invoice number and what the invoice was for. This will make reviewing transactions easier down the line.

Accounts payable is credited and the outstanding balance increases.

The account that’s debited is likely inventory, or anything similar that you use in your accounting.

Entering an invoice payment

On the 15th of the month, you pay the invoice in full.

Accounts payable is debited, decreasing the outstanding balance.

Credit the account that reflects the invoice payment method. For example, if you pay by ACH credit, you credit your bank account.

Between the purchase and payment, the credits and debits offset each other and the balance is reduced to zero.

Reversing a voided invoice

Soon after invoicing you, your supplier informs you that they have to cancel the order and will void the invoice.

You receive confirmation that the invoice was voided on April 5th.

The transaction is essentially entering an invoice in reverse.

You debit accounts payable and credit the payment account.

The effect of this is “undoing” the original invoice entry.

The crediting and debiting of each account negates any change in balance between the two transactions.

Adjusting an invoice amount

Instead of canceling the order and voiding the invoice, your supplier reaches out and mentions they can’t fulfill part of the order with a value of $500.

They send over an adjusted invoice on April 5th.

If they adjust the invoice and it’s the same invoice number, the process is similar to reversing an invoice with one key difference: the debits and credits are not for the full invoice amount.

If it’s a brand new invoice with a new invoice number, you may want to create a reversal transaction and then enter in the new invoice.

This would be two separate transactions.

Adding late fees and interest

The month passes and you forgot to pay the invoice.

The supplier’s late policy is a $100 late fee and 3% interest on the invoice amount ($300 for a $10,000 invoice).

This is the first example where we need to split one side of the transaction into multiple parts.

When doing this, always remember that the debits and credits must be equal.

Let’s start with the debits.

There will now be two debits: one for the interest amount and one for the late fees.

The interest expense ($300) and late fee ($100) add up to $400.

This means the credit must be $400, all of which is run through the accounts payable account.

Accounts payable journal entry mistakes to avoid

Whether you’re an experienced expert or new to accounting, honest mistakes can happen. Look out for these common errors and take our tips to help avoid them.

Data entry errors

The simplest error you can make with a journal entry is inputting the information incorrectly.

Whether it’s a date, amount, or description, these have a waterfall effect that can lead to duplicate entries and inaccurate balances.

Avoid this by:

- Using Optical Character Recognition (OCR) technology to verify data from scanned or digital invoices

- Having a second person review the entry before posting

- Auditing your accounts payable ledger regularly

Incorrect account errors

It can be ambiguous which account each line item in an invoice is connected to.

Similarly, it’s easy to make a mistake when marking which account a payment came from, especially if payments come from multiple bank accounts or credit cards.

Both can throw off your accounting and trigger a need to audit the books, an unnecessary time sink.

Avoid this by:

- Using invoice coding to embed essential information into an invoice

- Marking the payment account on the invoice once it’s been paid

- Including the team that’s responsible for the purchase to confirm details (e.g. the marketing team for an invoice of an advertisement shoot)

Entry reversal errors

Entry reversal refers to having the debits and credits reversed.

As a result, the balances are moving in the opposite direction than was intended, potentially making the business look more in debt than it is.

Avoid this by:

- Confirming balances after making any amount of journal entries

- Entering debits and credits first, then reviewing them after entering the rest of the information

Improving how you track accounts payable with BILL

An accounts payable ledger helps you stay on top of outstanding invoices and payments.

But with its dependence on manual entries, it’s still prone to errors and takes work to keep up-to-date.

With BILL, manual entries are a thing of the past.

The platform syncs with your accounting software so invoices, payments, and adjustments are all entered automatically.

Try BILL for yourself and see how we save AP teams an average of 50% of their time by streamlining every step of the accounts payable process.