Accounts payable seems like a pretty simple and straightforward process.

You receive an invoice from a supplier or contractor, match it up against work done, and then get it paid.

Unfortunately, real life is a little more complex than that.

Some invoices are purchase order-based, while others aren’t.

Some come from one-off suppliers, others from regular vendors.

Refunds and credits have to be issued on occasion, and documents and records must be filed in a particular manner to maintain compliance with local legislation.

For all of these intricacies, you need an accounts payable policy.

An accounts payable policy will help you maintain a standard payment process, reduce fraud, and keep your team on the same page.

Whether you’re creating an AP policy for the first time or worried that your current policy is missing some important pieces, keep reading to learn the ins and outs of building an effective accounts payable policy.

What is an accounts payable policy?

Your accounts payable policy is the set of guidelines and procedures your organization establishes and follows to manage outstanding debts to suppliers and contractors (known as accounts payable).

AP policies vary between companies but commonly include rules and processes to follow with regard to invoice processing and payment, record-keeping, and approval workflows.

How the accounts payable policy fits within your AP workflow

Your accounts payable policy is one part of the general AP workflow.

The accounts payable workflow details the complete end-to-end process from procurement through to payment and close-out, usually documented as a flowchart.

Your AP policy describes the regulations and processes to follow and the requirements that must be met as part of that workflow.

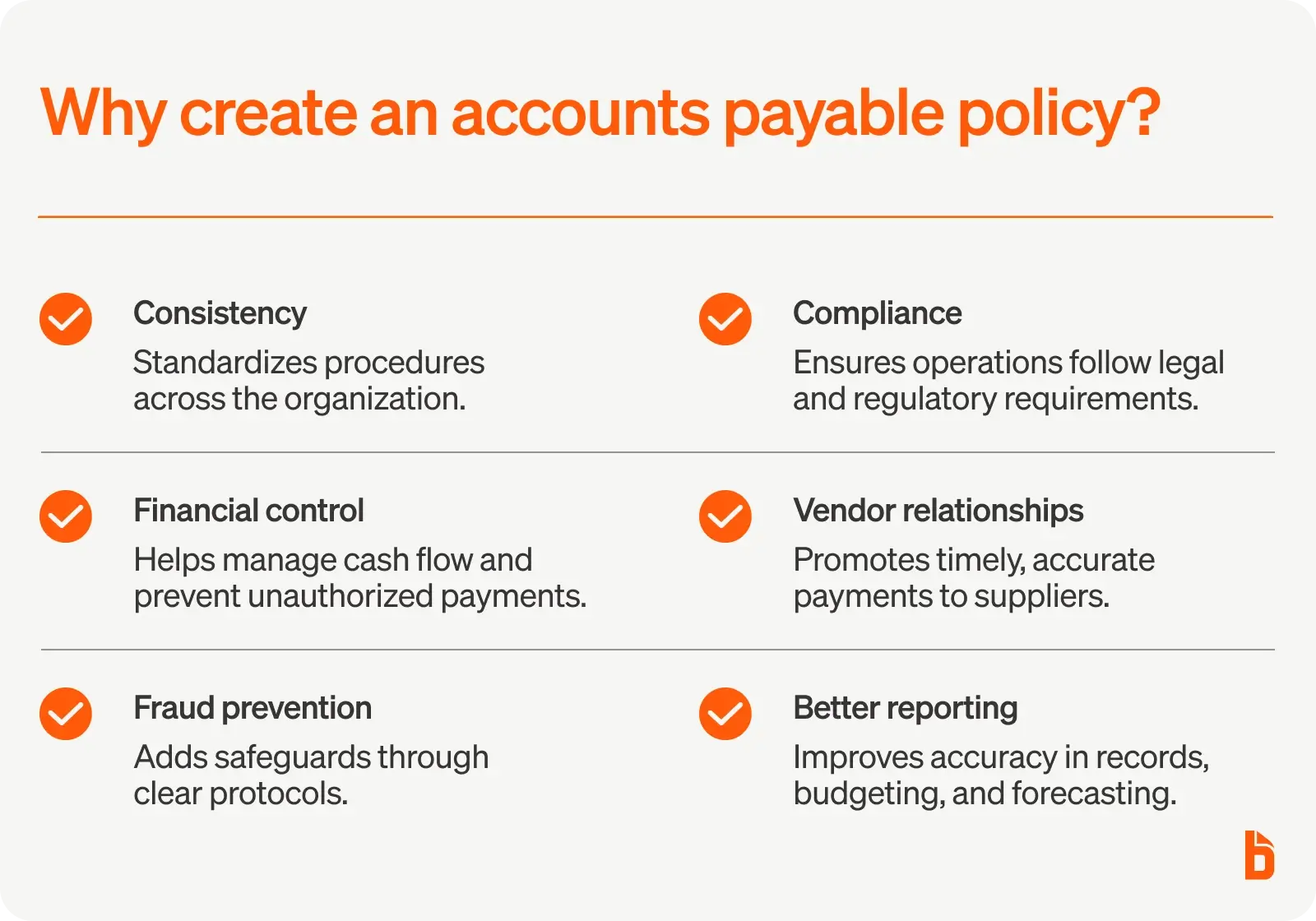

Why should you create an accounts payable policy?

Documenting and distributing an accounts payable policy provides several important benefits:

- Consistency: An AP policy establishes standardized procedures and workflows that all must follow, creating consistency across the organization.

- Financial control: AP policies set clear guidelines for payment terms and approvals, creating positive effects for managing cashflow, maintaining accurate records, and preventing unauthorized payments.

- Fraud prevention: Well-designed accounts payable policies reduce fraud through detailed controls and protocols.

- Compliance and risk management: Your accounts payable policy ensures that AP team members operate within legal and regulatory frameworks, reducing legal and financial risk.

- Stronger vendor relationships: AP policies include guidelines regarding payment terms, so your company can make timely and accurate payments, keeping suppliers happy.

- Better reporting: When AP policies are followed correctly, records are more accurate and detailed and include fewer errors, improving the company’s financial reporting, ability to budget, forecast, and make strategic decisions for future growth.

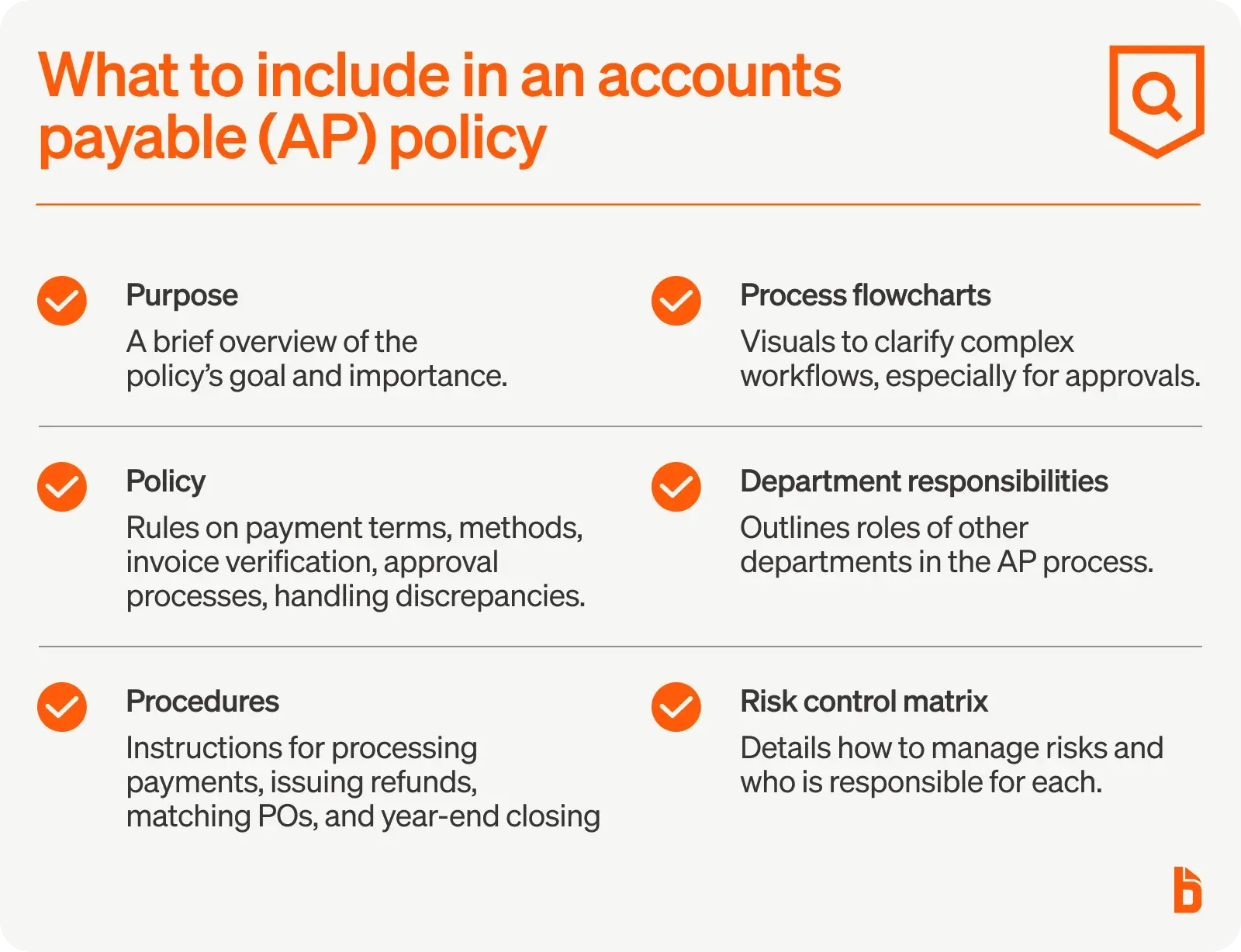

What should you include in your AP policy?

Every organization’s accounts payable policy looks slightly different.

There is no “one size fits all” solution.

That said, when you examine the policies of various companies and institutions, you do start to observe some common trends. All of them outline the common procedures an AP team follows, for instance.

So, while the below doesn’t constitute a list of “must-have” sections for your accounts payable policy, it is a series of suggestions or ideas to get you started, inspired by real-life AP policies from the likes of the University of Iowa and the United Nations Population Fund.

The first three (Purpose, Policy, and Procedures) are the most commonly observed subheadings.

Purpose

The first section of your accounts payable policy outlines the broad purpose of the document to come.

For example, here’s what Hudson County Community College states in its AP policy:

Policy

In the second section, you’ll list the specific policies your accounts payable department holds.

Here’s an example of one specific policy from the United Nations Population Fund:

Common examples of policies to detail in this section include:

- Payment terms

- Available payment methods

- Check processing

- Refunds and credits

- The verification of invoices prior to payment

- The use of checklists (such as a Payment Request Checklist)

- Segregation of responsibilities

- Correct methods of approval

- Resolving discrepancies

Procedures

Your procedures section details the specific processes the members of your accounts payable department are to follow to complete certain tasks.

For example, the United Nations Population Fund includes a four-step workflow for the processing of purchase order-based payments:

Some of the most common procedures you’ll find in AP policies include:

- How to process a purchase order based payment

- How to properly file accounts payable documentation

- How to process a check

- How to issue a refund

- How to issue a credit memo

- How to close out the fiscal year-end

- How to issue purchase orders

- How to match invoices with purchase order numbers

- How to handle advance payments to vendors

Process overview flowcharts

Flowcharts are a helpful way to illustrate AP processes in a visual manner.

They are commonly used to illustrate approval workflows, which can be complex and vary depending on factors such as department, invoice amount, and whether or not a PO number is present.

Here’s how the United Nations Population Fund uses flowcharts in their accounts payable policy document:

Department responsibility

The department responsibility section of your AP policy briefly describes the obligations of various non-AP departments within your organization as they relate to invoice processing, purchase orders, and payment processing.

Macomb Township provides a helpful example:

Risk control matrix

Some AP policies include a risk control matrix that describes how different risks should be handled and by whom.

The below is an example from the United Nations Population Fund:

Free accounts payable policy template

You can use the below template as a starting point for your own accounts payable policy.

Remember, though, that every organization has its own needs, meaning there is no AP policy to end all AP policies.

Here are some AP policies for inspiration:

- Hudson County Community College

- United Nations Population Fund

- University of Iowa

- Macomb Township

- Morehouse School of Medicine

Ready to automate your accounts payable process?

Your accounts payable policy is critical to making sure your suppliers are paid on time and for protecting your organization from fraud risk and shadow spending.

A clearly written and easily accessible AP policy document is a good start. To ensure your team follows processes to the letter, however, you need an accounts payable system that automates many of the most time-consuming steps—like BILL.

BILL saves you time by helping you:

- Automatically import invoices

- Simplify your approval processes

- Pay invoices by ACH, credit card, check, or international wire transfer

- Integrate with the rest of your AP tech stack to keep data synced

Whether you’re building your accounts payable policy for the first time or just looking for ways to improve what you’re doing right now, find out how BILL can help.