Businesses strive to earn high profits—but to do that, they need to know the minimum revenue required to keep operations afloat, or in other words, to break even.

What is a break-even analysis?

A break-even analysis can help you determine where that point lies. Calculating a break-even analysis is also crucial for determining if a venture is worth pursuing, in optimizing your pricing strategy, and simply in understanding what level of sales your company will make a profit at.

The ins and outs of a break-even analysis

A break-even analysis (not to be mistaken for the margin of safety) determines the production level where a venture makes neither a profit nor a loss. It’s a financial calculation that helps you determine the number of units you need to sell to cover business costs.

The break-even calculation weighs the cost of a new business, product, or service against each unit’s selling price to determine where total expenses and revenue are equal.

For example, if you start a landscaping maintenance business, you’ll need to finance fixed assets and operational expenses. Some of your fixed assets will be a van, a lawn mower, and other equipment. Operating expenses may include advertising, fuel costs for your equipment, and labor, to name a few.

Let’s say that your total expenditure is $10,000 a month.

A break-even analysis shows how many lawns you must maintain to generate $10,000 in monthly revenue.

If you bring in $500 in sales revenue for each landscaping job, you’ll need to maintain 20 properties per month—that’s your break-even point. At that point, your revenue from sales will cover the operational costs.

But there’s more to using this financial analysis tool. In addition to determining how many goods or services you need, a break-even analysis shows you the point at which your company will be profitable.

When to conduct a break-even analysis

You don’t have to perform a break-even analysis at a specific point in your business’s life. Instead, it’s smarter to run a break-even analysis at various business stages. Here are a few essential timeframes ripe for a break-even analysis for your business.

Starting a new business

You should include a break-even analysis when creating a business plan for a new venture.

A projection about the revenue needed to break even enables you to gauge if starting a new business is feasible. The margins for some companies are so low that trying to generate the required revenue may not be worth the effort.

Consider a break-even analysis as a cash forecast, showing the business model’s viability. Knowing the revenue required to break even helps you determine your pricing strategy. Additionally, you can use a break-even analysis to estimate how long it will take for your business venture to become profitable.

Launching a new product

Ideally, it would be best if you did a break-even analysis for each product or service offered. Simply using average costs and selling prices per item doesn’t help you gauge each product’s or service’s impact on your financial standing.

That’s because additional products usually add more expenses and may even increase your total fixed costs. The analysis will help determine if you can afford to stock the new product. You’ll also learn what the selling price needs to be to break even.

Changing a business model

Global lockdowns have changed the way many businesses offer their products and services. The number of employees opting for remote work increased drastically, especially while many services have moved online.

Changing your business model has a direct impact on your expenses. For example, you won’t incur rental or storage costs if you move inventory out of your warehouse and opt for drop shipping. An expense reduction influences the revenue required to break even and may even enable you to lower prices.

Lowering pricing

You may decide to lower your prices to generate higher sales. When reducing costs, you need to determine how many additional units you need to sell to offset the price decrease. In other words, is it beneficial or harmful to your business if you decide to lower prices? What kind of projections might you see if you do offer lower prices?

Why break-even analysis matters

Calculating a break-even analysis requires you to account for fixed and variable costs relative to the unit price. Fixed costs remain the same, regardless of the number of units sold. Variable costs fluctuate since they are dependent on sales, but they are the total labor and material costs required to produce one unit of product.

- Fixed costs: Rent, insurance, and permanent labor

- Variable costs: Hourly labor, sales commission, and materials costs

Companies with low fixed costs usually have a low break-even point—but only if variable costs aren’t higher than sales. And while you can lower your break-even point by reducing costs or raising prices, you shouldn’t do either before examining internal and external factors.

Lowering your material costs may result in low-quality products, harming your brand. On the other hand, increasing the prices of products similar to your competitors’ could decrease sales. Using a break-even calculation, you dive deeper into how pricing and production costs impact your business’s ability to sustain itself.

Formula to calculate the break-even point

Calculating a business’ break-even point is the fixed costs divided by the sales price per unit minus the variable cost per unit. This is the formula for calculating the break-even point in units of a product sold.

Break-even point = Fixed costs / (Sales price per unit – Variable cost per unit)

Let’s draw an example: Say a taco food truck has $1,000 in fixed monthly costs. The company spends $3 to make a taco, and it sells each taco for $7.

Using the break-even formula, you can see that the food truck needs to sell 250 tacos every month to break even. Anything they sell beyond 250 will generate a profit.

$1,000 / ($7-$3) = 250 units

That formula shows you how to find the minimum number of units you need to sell to break even. But you can also use a different formula to determine how much you need to earn in sales to break even.

Note that this formula for calculating the break-even point in sales dollars also includes the contribution margin and the contribution ratio. Let’s dive into those next.

The contribution margin

The contribution margin is valuable because it shows how much is left to cover fixed costs after removing the variable costs. You find the total contribution margin by subtracting the total variable expenses (V) from the total revenue (R).

Contribution margin = R – V

You can use the same formula per unit to find the dollar contribution for each product or service sale. But instead of using total sales revenue minus total variable costs, you would subtract the total variable cost per unit from the sales price per unit.

Let’s say the taco truck has variable costs of hourly pay and material costs totaling $2,000 per month. Assuming they sell 500 tacos a month, they have a revenue of $3,500 when they charge $7 per taco. You would plug in those numbers and find this as their contribution margin:

$3,500 – $2,000 = $1,500

According to this calculation, the taco truck has a $1,500 contribution margin.

The contribution ratio

It’s also helpful to see this figure as a percentage—which is where the contribution ratio comes in. It reveals the percentage of your company’s sales income to pay for fixed costs.

The contribution ratio is total revenue minus total variable expenses, divided by the total revenue.

Contribution ratio = (R – V) / R

Using the taco truck as an example, we can plug in their numbers as such:

$3,500 (R) – $2,000 (V) / $3,500 (R) = 43%

Generally speaking, a good contribution ratio is 50%-60%. With a 43% ratio, the taco truck should probably lower their variable expenses where possible or see if they can charge $10 for their tacos to see a higher percentage.

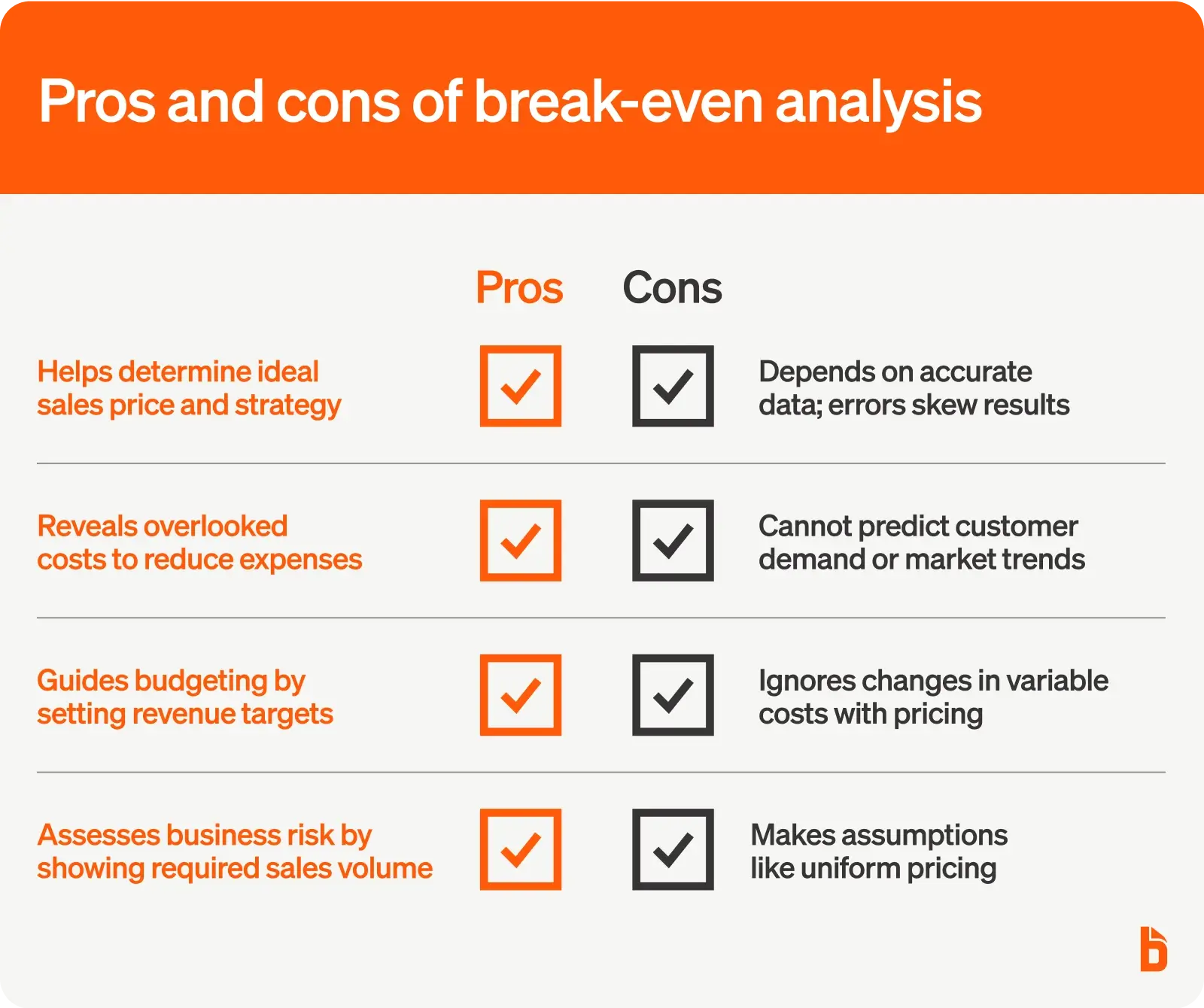

The benefits of calculating a break-even point analysis

As a business owner, you must examine all the factors influencing your costs and revenue. A break-even analysis helps you do just that—and more. It further sheds a light on smarter pricing, helps to identify overlooked costs, allows you to create a better budget, and accurately gauges risk.

Benefit #1: Determines better pricing

Knowing the break-even point helps you to determine the ideal sales price. Once you choose your break-even price, you can incorporate customer pricing into your strategy.

If you’ve determined that the product’s selling price needs to be $5 to break even, analyze the impact on your financials if you lowered it to $4.99. The difference of one cent makes the product appear significantly cheaper to some customers, who may be more likely to buy it.

Benefit #2: Identifies overlooked costs

The break-even analysis helps you identify all the negligible costs involved in the production that may be overlooked.

For example, a full-time employee may have insufficient work to fill the whole day so that they could become an hourly laborer. Excessive material might be used, which needs to be reduced. Your driver could be taking the long route for deliveries. Once you identify overlooked costs, you can make changes to help lower your break-even point and increase profits.

Benefit #3: Helps with budgeting

It’s vital for businesses to know how much revenue they need to generate and the expenses involved to be profitable.

If you’re not generating enough profit, you can make business decisions to boost revenue or decrease costs. For instance, you may need to increase your advertising budget to attract more sales if it’s challenging to generate the revenue you need to make a profit or draw a salary.

Benefit #4: Gauges risk

The break-even analysis can show you if the venture is worth pursuing by helping determine the level of risk of actually starting the business. How? It gives insight into your return on investment (ROI) by guiding the sales volume required for your business to remain operational.

If the analysis reveals a higher number of clients needed to break even than you expect to attract, that could lead to business failure. You may expect customer growth as the business progresses, so the analysis reveals the additional funding you’ll need to stay in business.

Limitations of a break-even analysis

While calculating the break-even point can drive strategic pricing and help you better manage business finances, there are limits to what a break-even analysis can do. That’s why you shouldn’t solely rely on a break-even analysis to help determine aspects or make decisions about your business, but instead, use it as a helpful tool.

Limitation #1: Highly dependent on accurate data

Even with the best eyes, it’s easy to overlook or underestimate certain expenses, and incorrect data can skew the entire analysis.

Limitation #2: Cannot predict demand

While the analysis can help you identify the sales needed to break even, it cannot gauge demand for your product or service. You should consider forecasting methods if you’d like to understand your business’s outlook better.

Limitation #3: Doesn’t consider variables

Lowering your price to sell more units may decrease your variable expenses. Learn how you can reduce expenses like this without harming your business.

Limitation #4: Makes assumptions

The formula is easier if you assume a business sells all its units at the same price. If you want to account for discounts, you can adjust your break-even analysis to include a tiered pricing structure.

Determine your business’s break-even point with BILL Spend and Expense

Doing a break-even analysis provides several benefits—but above all, it helps you mitigate risk and avoid losing money with an unprofitable business idea.

Of course, compiling a break-even analysis requires processing invoices, expense reports, and dozens of other necessary paperwork, data entry, and predictions. That’s why most business owners opt for software that seamlessly processes essential data, like variable costs and documents, all in one place.