A cash flow budget helps you time your income and expenses to ensure you’ll have enough money from week to week. It looks at cash only, which in business terms refers to cash payments and the money available in any associated bank accounts.

Cash flow is a unique budgeting method because the focus is on cash on hand rather than profit. Here’s what you need to know about cash flow budgeting.

The ins and outs of cash flow budgeting

Cash-flow budgeting looks at what money is coming in (cash inflows) vs. what money is going out (cash outflows). It zeroes in on cash flow to ensure that your business has enough income to cover expenses. This is different from a budget you might create to meet specific business goals.

You might use both long-term and short-term budgeting within your cash flow budget.

Short-term budgeting allows you to keep a close eye on your cash flow and upcoming goals and expenses. In contrast, long-term budgeting looks at a year or more into the future, and this view enables your business to make cash flow adjustments if needed.

Ultimately, this method asks, “Will my business have enough money to continue its operations in both the short-term and long-term?” After preparing a budgeting sheet, the cash flow bottom line answers this question.

It’s an excellent technique for all business sizes because it forces business owners to look at their financial plans for the next couple of months (short-term) to several years (long-term) or anytime in between.

Why you should use cash flow budgeting

Your profit and loss statement (P&L) doesn’t always reveal how much money your business has to spend. A cash flow projection can help to learn how much you’ll have available after you pay your bills, and whether you’ll have enough cash to cover your operating expenses, loan payments, and other costs.

Knowing your cash inflow is essential. If a company isn’t bringing in enough profits, it can still rely on its cash inflow to stay afloat until solutions are implemented. If there isn’t any cash (i.e., a negative cash flow), then a company without enough cash will sink.

So while your statement shows that you may be experiencing a profit today, there’s no way to tell how things will go six months or a year from now. A cash flow budget helps you determine whether you’ll have enough to manage your finances and prepares you for business ups and downs.

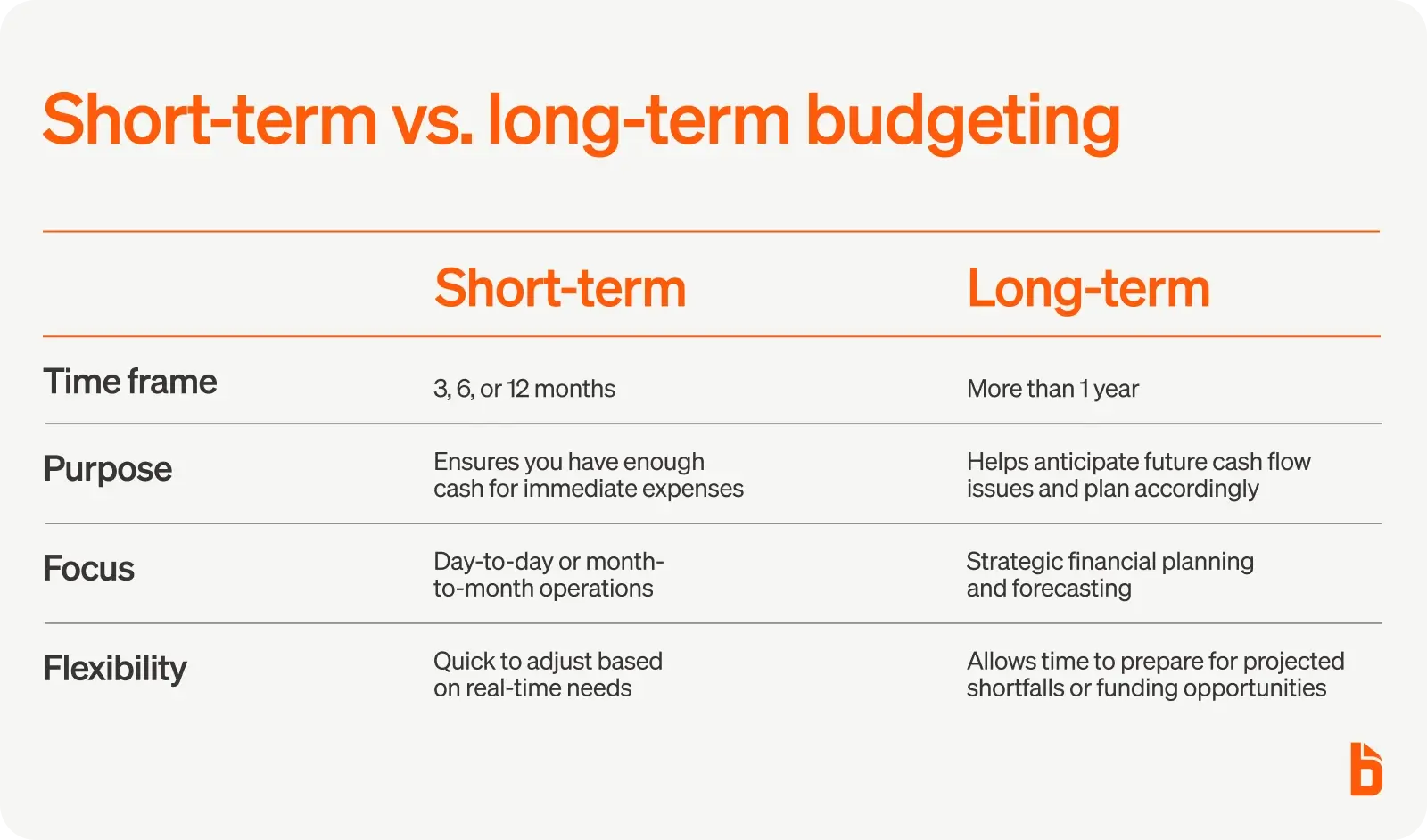

Short-term vs. long-term budgeting

Short-term budgeting covers fiscal periods from three, six, to twelve months at a time. It minimizes uncertainty by showing you whether you’ll have enough incoming cash for the next few months to a year.

This method is ideal for verifying that you have plenty of liquid cash to pay real-time expenses, such as payroll, utilities, rent, and any debts that may be due soon.

Long-term budgeting covers fiscal periods longer than one year. Preparing a long-term cash budget helps you recognize potential cash inflow or outflow problems so you can make changes now to ensure you have enough cash later.

If you see that your balance is less than your predicted expenses, then you have time to make adjustments. You can look into additional sources of income, make changes to your existing budget, or apply for a loan. (Applying for a loan with a long-term budgeting plan can also show the lender that you have a plan in place.)

How cash flow budgeting works

Since cash flow budgeting is a glance into your business’s future, you’ll need expense software as well as recent bank statements and budgeting plans. Here’s how to set up a cash flow budget:

Step #1: Determine your time frame

A typical cash flow budget is prepared from three months (short-term cash budgets) to a year (long-term cash budgets) in advance, although it’s also acceptable to create one every week, month, or quarter.

Step #2: Identify your projected cash flow

Your sales forecast estimates your expected sales revenue within a certain period. You can base this on previous sales forecasts.

Once you have an estimation, you can map out your sales forecast for the next few months (or however long your time frame is). Remember that the goal is to get an idea of the future, so be prepared for fluctuations.

Step #3: Input your current net cash flow

Since your business’s cash balance is liquid money, this number might be in a separate part of your budgeting sheet. Be sure to include savings, petty cash, and anything else in the bank.

Step #4: Analyze your cash inflow vs. outflow

Cash inflow includes all incoming money, including physical cash and credit that your customers use to pay.

Cash outflow includes any money that is leaving the business, like payroll, rent, insurance, utility bills, loan payments, and variable costs like one-time purchases, upgrades, and repairs.

Step #5: Calculate the ending cash balance

Add all your cash inflows and subtract your cash outflows from each month. The difference is your monthly cash balance. A positive cash flow means you’re in good shape, while a negative number will tell you that changes need to be made.

The great thing about a cash flow budget is that it can be applied to any situation and used alongside other business budgeting methods.

Is cash flow budgeting a good fit?

The cash flow budget method is a simple way to make sure you can make ends meet and save enough money for short- or long-term goals, which is why this method is so helpful for small- to medium-sized businesses.