Incremental budgeting is one of the most accessible business budgeting methods because it’s so easy to use. It’s also the most conservative—because the focus is on marginal changes, department managers can retain the financial status quo.

How do you know if incremental budgeting is right for your organization? Let’s look at how it works and why you might consider an incremental budget for your business.

The ins and outs of the incremental budgeting method

The incremental approach is ideal if you want simplicity and funding stability, but it’s not a good fit for every company.

A precursor to zero-based budgeting, businesses and government agencies have been using incremental budgets for decades. This budgeting method assumes that the current budget is more or less adequate, and only incremental adjustments are needed to create the next one.

With incremental budgeting, you or your accountant will prepare the next budget by making small changes to the current or prior period’s budget.

You will add to or subtract from the previous budget in order to include new quantities, new activities, or trend changes, whether financial, seasonal, or societal.

Where other methods might entail an extensive analysis of each line item to try and reduce costs or better understand the value created, the incremental budget is more straightforward.

The idea with incremental budgeting is to not rock the boat with every new budget so departments can count on consistent, predictable funding and operate without worrying about major changes.

How incremental budgeting works

Some budgeting types are more dynamic, while others involve simple adjustments.

Incremental budgeting falls in the latter category: To find the budget for future periods, you’ll simply use the numbers from the current period to estimate the starting point for the new budget period. Then, you can add or subtract incremental amounts to create your new budget.

For example, say that a company paid its employees a total of $400,000 in salaries last year. Next year, they will increase those employees’ wages by 10% and hire six new employees, who will receive a base salary of $25,000.

The formula for this year’s increase via incremental budgeting will read: Current period's budget = Previous year salary + % of increment on previous wage + Salary of new employees

An incremental budget works well for educational institutions, governments, and large organizations that allocate funds to departments or long-term project and are used to experiencing only minor changes throughout the fiscal year.

On the other hand, it’s not the most useful choice for small businesses that require a more flexible budgeting approach. This is because it doesn’t have room for changing circumstances, nor does it allow you to respond quickly to new conditions and innovative ideas.

Why use the incremental budgeting method?

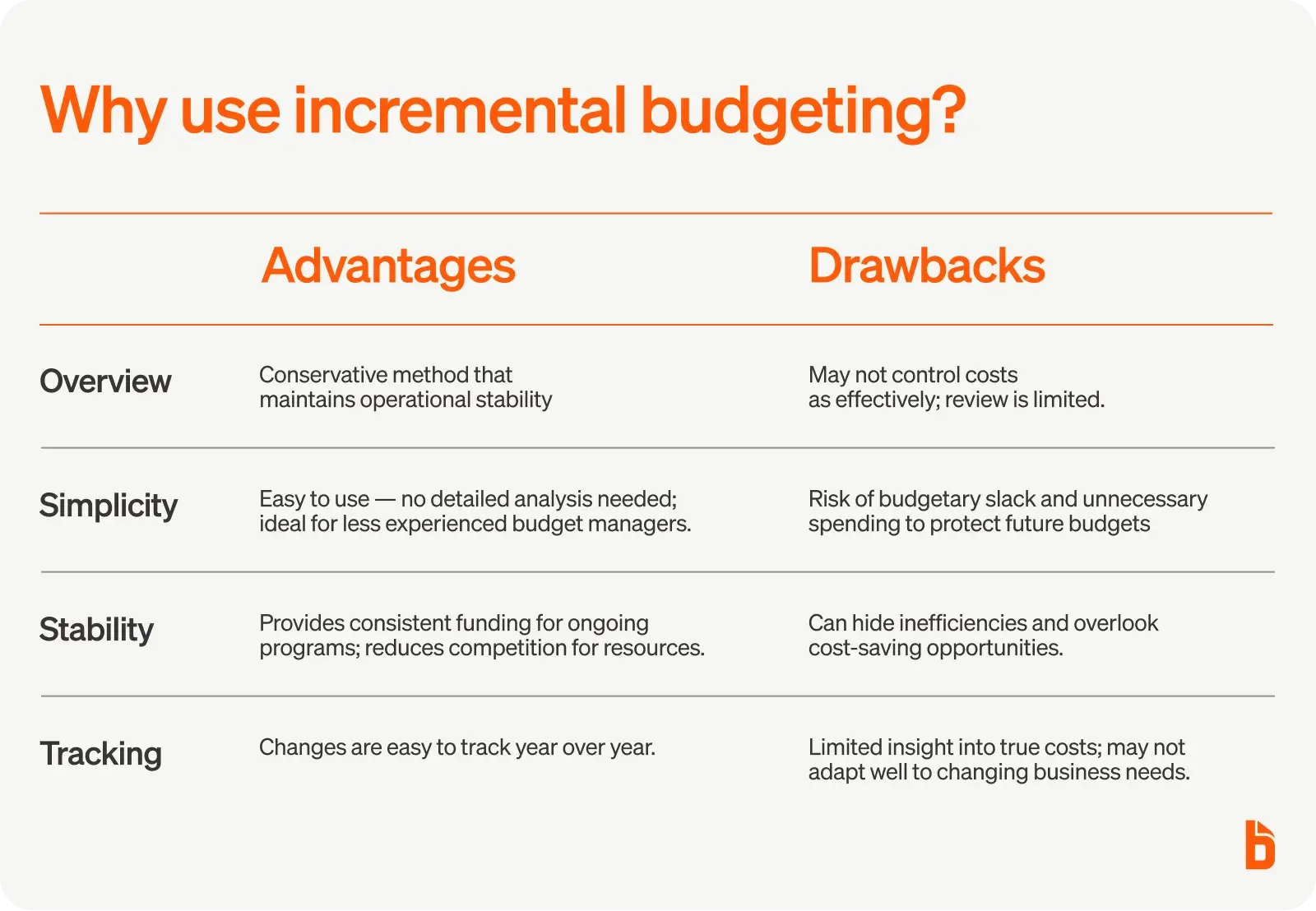

Incremental budgeting is a conservative method that helps businesses maintain operational stability. It’s also one of the easiest to prepare.

However, there are downsides, so be sure to look at the advantages and disadvantages of incremental budgeting to see if this method works well for your business format and goals.

Advantages:

- It’s easy to use: Incremental budgeting doesn’t require accountants’ detailed analysis or expertise. This method is easy to implement, even for business owners who don’t have a lot of experience with different budgeting techniques. Simplicity and consistency are the main advantages to using incremental budgeting.

- Provides stability throughout the company: Since it ensures that funds keep going to those programs that existed in previous budgets, there’s no need for managers to compete for funding or prove the value of their projects. This makes the incremental approach ideal for businesses with long-term projects requiring funding for multiple years.

- Change is simple to track: Since budgets typically remain steady year after year, business owners can easily see the impact of small changes on their projects and departments.

Drawbacks:

- May lead to extra spending: Since incremental budgeting adjusts based on the business’s needs each year, it’s not uncommon for departments to spend as much of their budget as possible to receive the same amount (if not more) the following fiscal year period. This, unfortunately, can lead to unnecessary spending without careful analysis.

- Budgetary slack: Although frowned upon, managers can make their department’s performance appear better than it is through either underestimating the amount of income or overestimating the number of expenses.

- Review of the budget is limited: Incremental budgeting doesn’t include an in-depth study of the budget, which means that many things can go overlooked. Instead, analysts or business owners may opt for other, more detailed budgeting methods, like activity-based or zero-based budgeting, to gain more clarity.

Make incremental budgeting work for your business

Incremental budgeting speaks to business owners because of its simple, easy-to-understand methodology and ease of tracking changes. Still, it can lead to adverse long-term effects, such as limited budget reviews, unnecessary spending, and budgetary slack implementation.

That’s why incremental budgeting is best for a larger, conservative business environment that benefits from a predictable budgeting process.