One of the most essential facts of business is that companies need capital to grow. For many companies, some of that capital comes from retained earnings—the portion of profits a company keeps instead of paying it out to shareholders.

As a key indicator of a company's financial performance over time, retained earnings are important to investors in gauging a company's financial health. This post will walk step by step through what retained earnings are, their importance, and provide an example.

What are retained earnings?

Simply put, retained earnings represent a company's accumulated net income that has not been distributed as dividends to shareholders. Some of the ways a company may use retained earnings include:

- Investing in research and development for the launch of a new product

- Merging with or acquiring competitors

- Paying debt obligations

- Hiring production staff to increase output

- Buying back company stock from the market (share buybacks)

Retained earnings: appropriated vs unappropriated

Retained earnings can be categorized as appropriated or unappropriated.

Appropriated retained earnings are those set aside for specific purposes, such as funding capital expenditures or paying off debt.

Unappropriated retained earnings have not been earmarked for anything in particular. They are generally available for distribution as dividends or reinvestment in the business.

What type of account is a retained earnings account?

A retained earnings account is an equity account. At the end of a given reporting period, any net income that is not paid out to shareholders is added to the business's retained earnings.

Net income vs retained earnings

Net income is the company's profit for an accounting period, calculated by subtracting operating expenses from sales revenue.

Retained earnings, on the other hand, represent the accumulated net income over multiple accounting periods that have not been paid out as dividends.

How to find retained earnings on a company's balance sheet

Retained earnings can be found in the shareholders' equity section of a company's balance sheet. It is typically listed as a separate line item, labeled “Retained Earnings” or “Accumulated Earnings.”

Are retained earnings an asset?

It's easy to mistake retained earnings for an asset because companies use them to buy inventory, equipment, and other assets. But a retained earnings account is reported on the balance sheet under the shareholders' equity, so they're treated as equity.

The company retains the money and reinvests it—shareholders only have a claim to it when the board approves a dividend.

Are retained earnings a debit or credit?

In accounting terms, retained earnings are a credit. They increase with a credit entry, and retained earnings decrease with a debit entry.

What is a statement of retained earnings?

A statement of retained earnings is a financial statement that shows the changes in a company's retained earnings balance over a specific accounting period.

For example, it might show the change in retained earnings over the past quarter or the past fiscal year.

What is on a retained earnings statement?

A retained earnings statement typically includes:

- The beginning balance of the company's retained earnings account

- Any net income or loss, cash dividends, or stock dividends

- The ending retained earnings balance

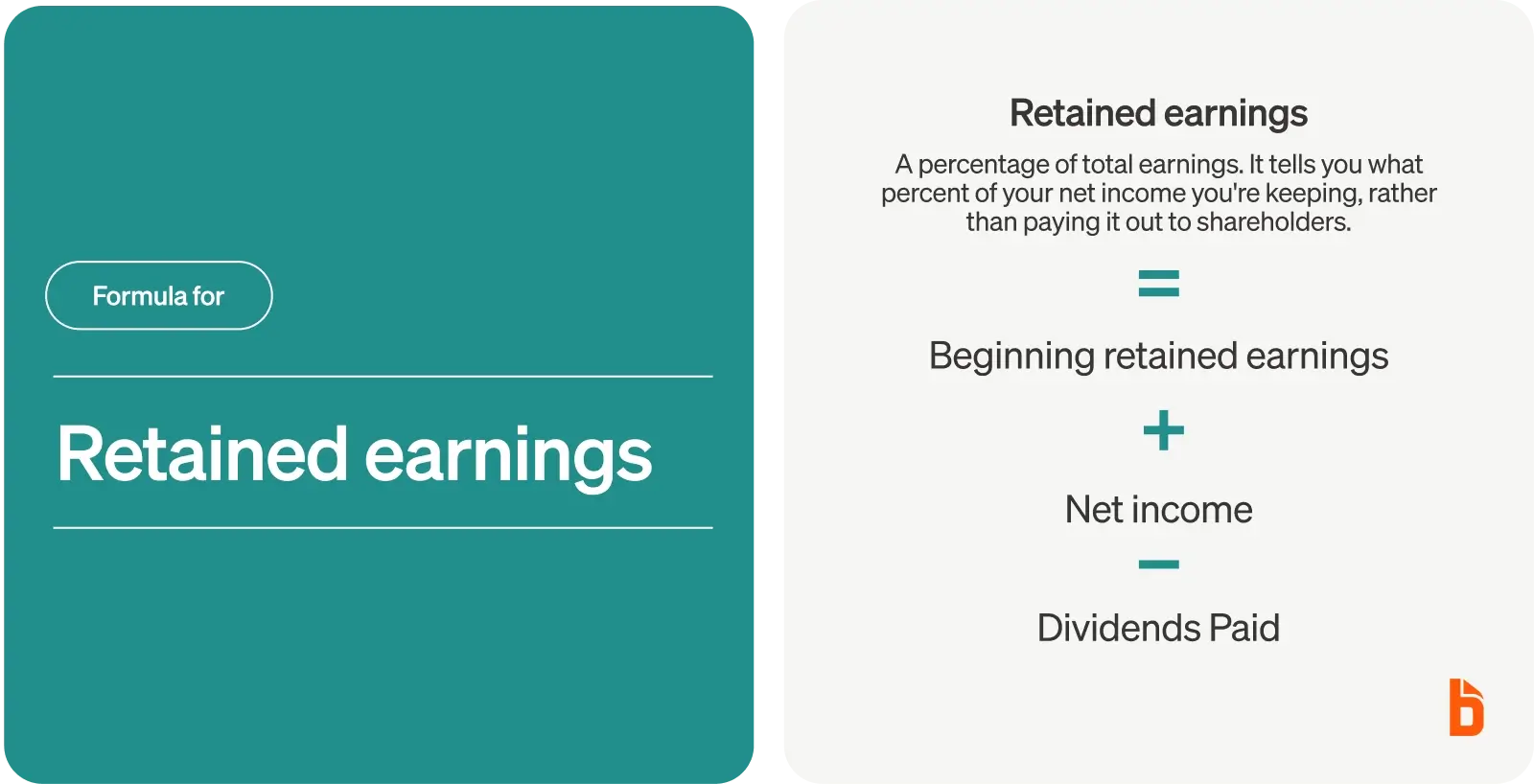

Retained earnings formula

Companies calculate retained earnings using the following retained earnings formula:

Ending Retained Earnings = Beginning Retained Earnings + Net Income – Dividends Paid

This formula takes the beginning retained earnings balance, adds the net income for the accounting period, and subtracts any dividends paid during that period.

Example of retained earnings statement with cash dividends paid

Consider a company with a beginning retained earnings balance of $100,000.

During the accounting period, the company generates a net income of $50,000 and pays cash dividends of $20,000, leaving it with $30,000 of its net income remaining.

That amount is added to the original $100,000 for a new total retained earnings of $130,000.

The company's statement of retained earnings would show that calculation:

$100,000 beginning balance + $50,000 net income – $20,000 cash dividends

= $130,000 ending retained earnings balance.

How to prepare a statement of retained earnings

Shareholders may also want to see a retained earnings statement. Let's get into the details of how to prepare this financial statement.

1. Provide a heading

Ensure you have a three-line header on a statement of retained earnings.

- First, mention the company's name.

- The second line should state ‘Statement of Retained Earnings.'

- The third line should depict the accounting period—for example: ‘For Year Ending 2021.'

2. Open with the balance from the previous year

The business retained earnings balance of the previous year is the opening balance of the current year. It's always the first line item.

You can find the amount on the balance sheet under shareholders' equity for the previous accounting period.

3. Include net income

Before you can include the net income in your statement of retained earnings, you need to prepare an income statement.

The income statement above should serve as an example. The net income amount in the above example is the net profit line item, which is $115,000.

4. Deduct dividend payments

Based on the amount of net income earned, your company might decide to pay a certain portion to shareholders as dividends. Some companies don't have dividend payouts—in that case, there's nothing to subtract.

Using the above example, you would subtract $35,000 for dividend payments.

5. Calculate the balance

After inputting all the figures, you'll be left with the total retained earnings for the year. That is your closing balance for the period.

What affects retained earnings?

As seen in the example above, the factors that directly affect the retained earnings calculation are the company's net income and any cash dividends that are paid out.

Indirectly, therefore, retained earnings are affected by anything that affects the company's net income, from operational efficiencies to new competitors in the market.

Can a company have negative retained earnings?

Yes, a company's financial statements may show negative retained earnings.

While negative retained earnings can be a warning sign regarding a company's financial health, an company's retained earnings can also be negative for a company with a long history of profitability. It simply means that the company has paid out more to its shareholders than it has reported in profits.

Is it good to have high retained earnings?

Generally, companies like to have positive net income and positive retained earnings, but this isn't a hard-and-fast rule. The decision to pay dividends or retain earnings for future capital expenditures depends on many factors.

Higher retained earnings may be a sign of a company's financial strength as it saves up funds to expand—or it could be a missed opportunity for paying dividends.

The best thing to do with a company's profits depends on factors that are unique to each company and its financial situation, including the business's financial health, business growth opportunities, cash flow issues, and so on.

What is the importance of retained earnings?

Retained earnings provide you with insight into your cumulative net earnings. But several financial statements need to be prepared to calculate retained earnings. One of them is the income statement, and you'll need to process expenses to put this statement together.

The simplest way to know your company's financial position is with an expense management platform that tracks operational activities in one place.

BILL Spend & Expense simplifies the invoice capturing process by doing all the hard work. All you have to do is review and approve.

Start managing your retained earnings with BILL Spend & Expense today!