Understanding how to calculate retained earnings is essential for business owners and investors alike, as it provides valuable insight into a company's financial health and growth potential.

This post will guide you through the process of calculating your company's retained earnings step by step to help you make informed decisions about your business's financial performance.

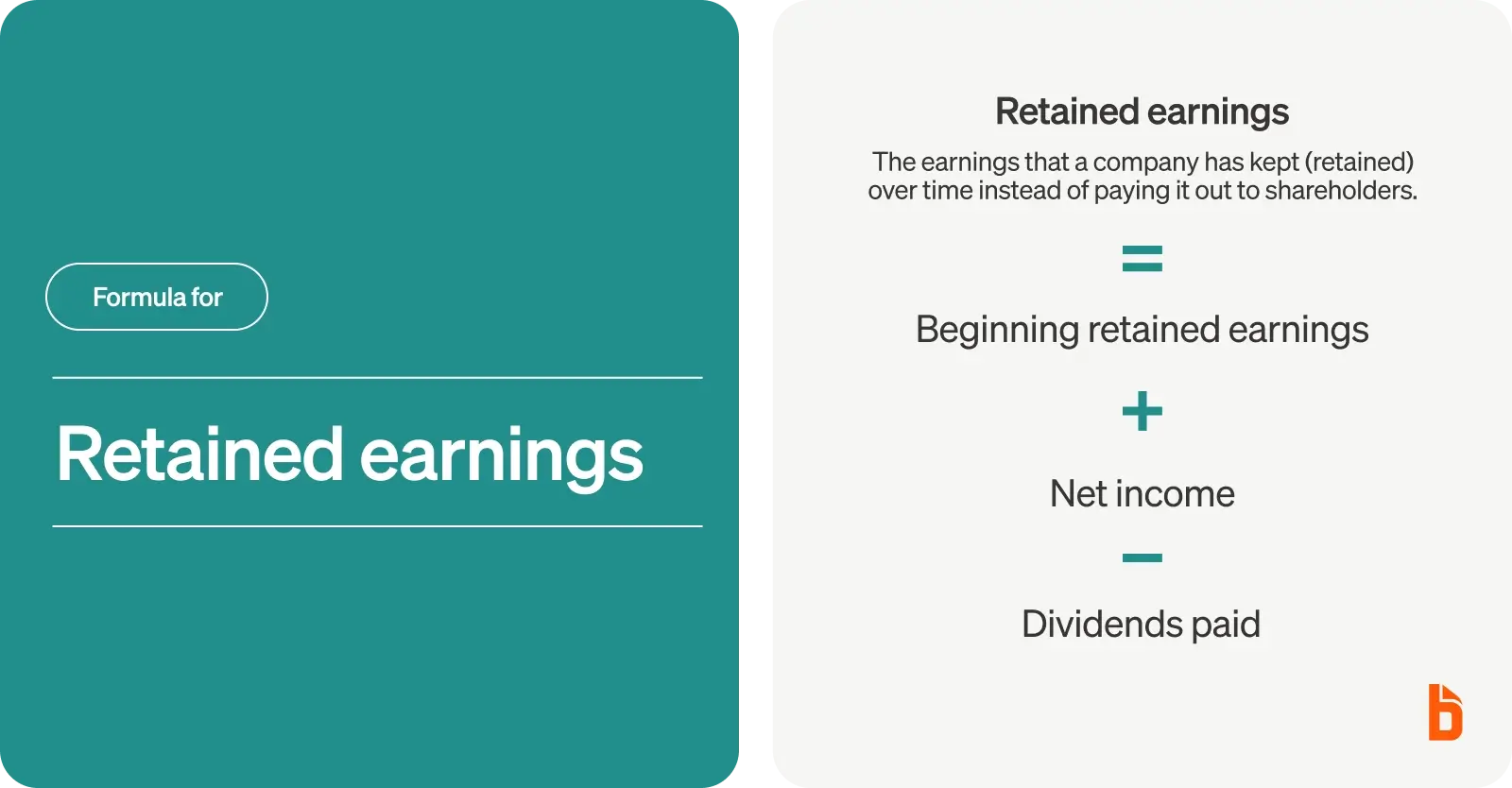

Retained earnings formula

Since retained earnings is a company's accumulated net income that's kept after paying out dividends to shareholders, you can find retained earnings with three factors:

- Beginning period retained earnings - This is the value of retained earnings at the beginning of the reporting period which can be found on a balance sheet.

- Net income (profit or loss) - The difference between a business’s revenues and expenses in the reporting period which can be found on an income statement.

- Dividends paid - Any amounts of the profits that are paid out to shareholders, typically on an annual or quarterly basis.

Given that, the retained earnings equation is as follows:

Ending retained earnings = Beginning retained earnings + Net income – Dividends paid

It's easy to understand the math if you think about what retained earnings actually are—the earnings that a company has kept (retained) over time instead of paying it out to shareholders.

So, you start with what you already had—the retained earnings the last time you calculated it. Then, you add any new net income since then, and subtract any dividends you've paid out since then.

What's left is your new retained earnings.

The formal structure is presented below, but that's the gist of it. You're just figuring out how much you've earned that you haven't paid out to your shareholders as dividend payments.

How to calculate retained earnings

Here's how to calculate retained earnings step by step:

1. Start with the beginning balance of your retained earnings

Retained earnings are found in the equity section of the balance sheet.

Balance sheets report the balance of accounts at a point in time. This means you’ll need the balance sheet that corresponds with the day before the period of time you’re looking at. If you’re looking to calculate retained earnings for the month of April, you’ll need the balance sheet ending on March 31.

2. Add your net income from the reporting period

Net income is reported on the income statement (or profit and loss statement).

You’ll need an income statement (or a revenue and expense report) that covers the beginning to the end of the reporting period. For the month of April, this means a report covering April 1 to 30.

Add this value to your beginning net earnings before moving to the next step.

3. Subtract any dividends paid out of the net income

Dividends paid are any amounts paid out to shareholders based on the shares owned, typically on a quarterly basis.

If there were no dividends paid out, you don’t need to do any other adjustments from step two. Otherwise, subtract the full amount of dividends paid from the amount calculated in step two.

Once this is done, you’re left with the latest retained earnings amount.

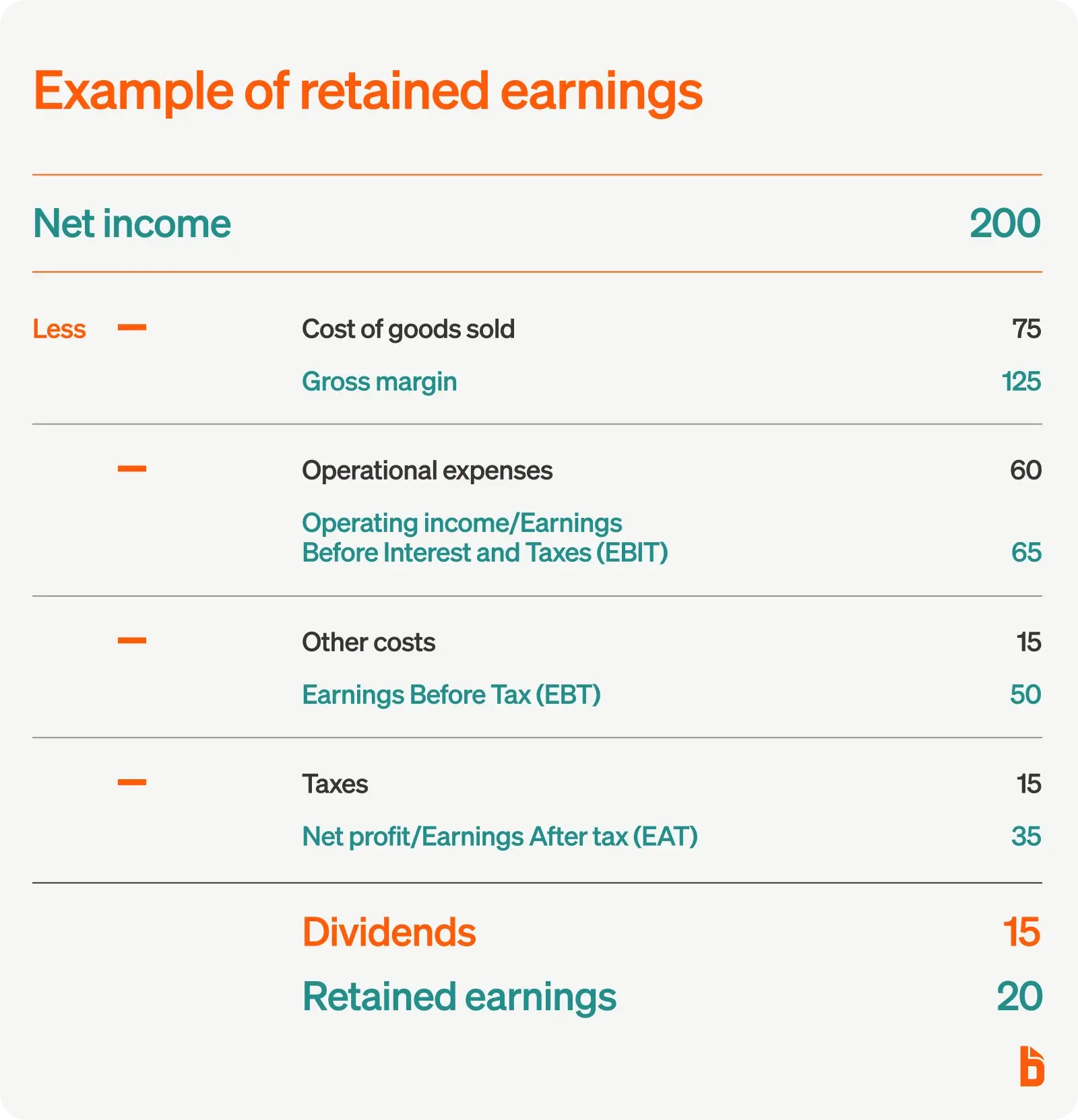

Example of retained earnings calculation

Let's look at an example to see how the retained earnings formula works.

Company XYZ has reported figures for a three-month period ending February 28, 2025 (figures are in thousands of dollars). While calculating retained earnings of this company, assume the beginning retained earnings balance is $0.

Plug the numbers from the example into the retained earnings formula:

Beginning period retained earnings + Net income (profit or loss) – Dividends paid

$0 + $35 – $15 = $20

Company XYZ's retained earnings are $20.

Nothing you'd write home about, but hey, it's just an example. If you multiplied each of those numbers by 1 million, it would work the same way.

$0 + $35 million – $15 million = $20 million

Now your company's balance sheet is looking pretty great—especially that shareholders equity section. It might be time to turn more of your company's net income into some dividend payouts!

Statement of retained earnings template

A statement of retained earnings template generally includes the following sections:

- Beginning Retained Earnings

- Net Income (or Loss)

- Cash Dividends

- Stock Dividends

- Ending Retained Earnings

In other words, it follows the retained earnings formula.

- The retained earnings you started with

- Your net income or loss since the last time you calculated retained earnings

- Any dividends you paid out

- Your new retained earnings total

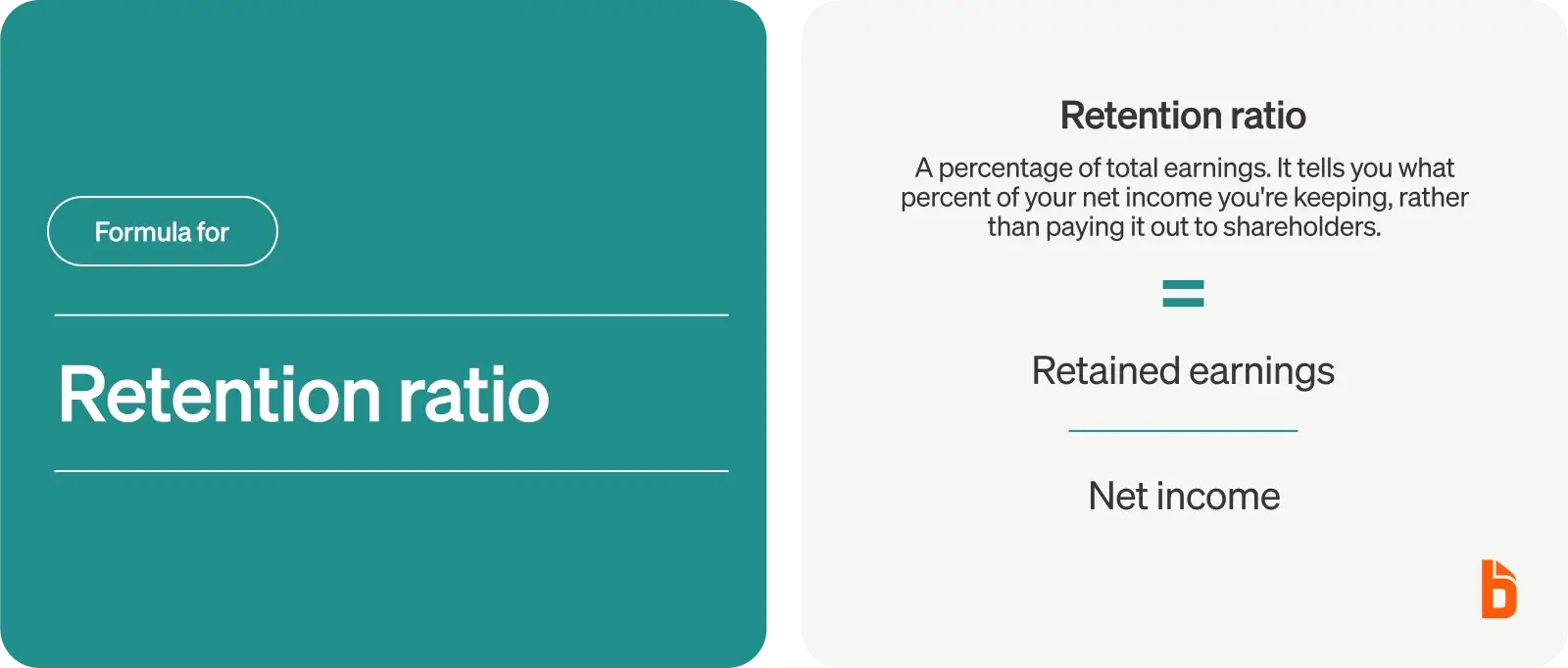

Retention ratio

Retained earnings can also be reported as a percentage of total earnings, known as a retention ratio.

In other words, it tells you what percent of your net income you're keeping, rather than paying it out to shareholders.

Retained earnings retention ratio formula

Here's how you calculate the retention ratio:

Retention ratio

Retained Earnings / Net Income

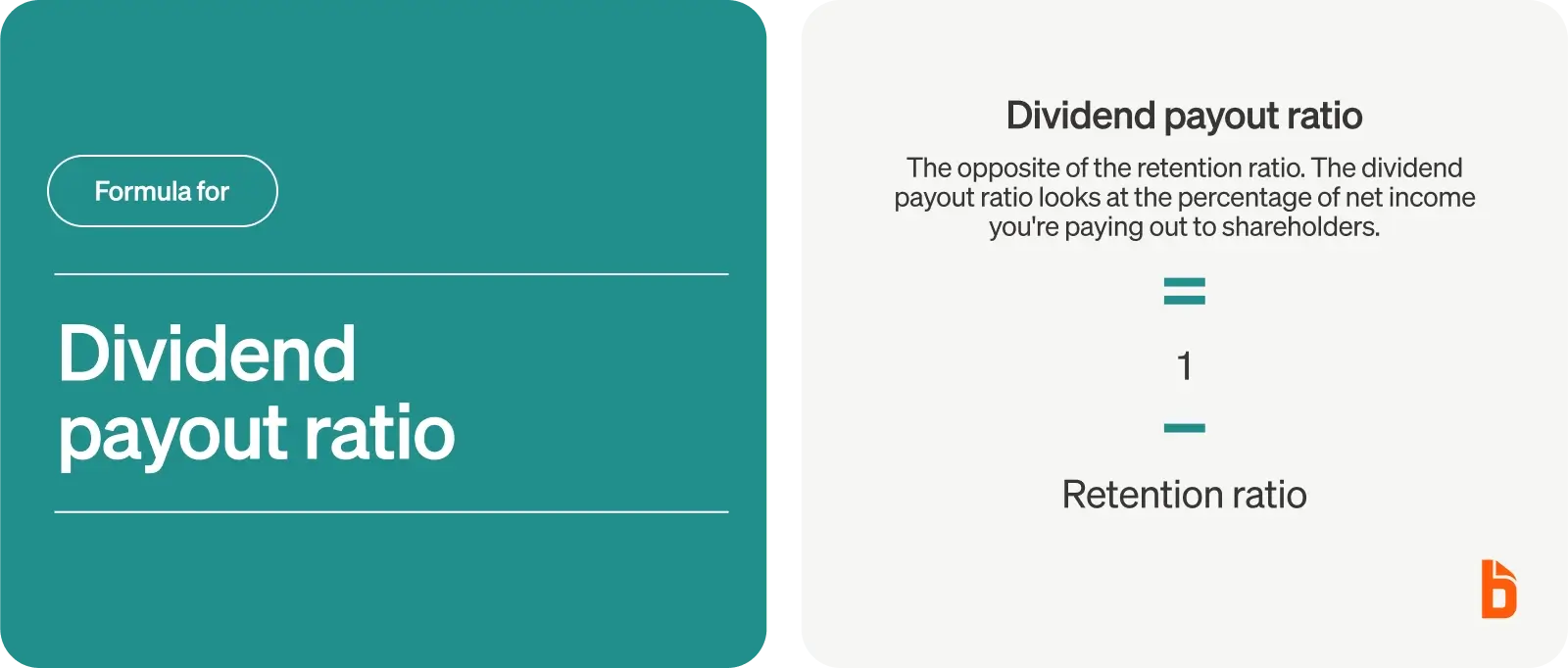

Dividend payout ratio

The dividend payout ratio is the opposite of the retention ratio.

While the retention ratio looks at the percentage of net income you're keeping, the dividend payout ratio looks at the percentage of net income you're paying out to shareholders.

You can find the dividend payout ratio by subtracting the retention ratio percentage from 100%. For example, if your retention ratio is 25%, then your dividend payout ratio is 75%. You're keeping 25% of your net income and paying out the other 75%.

Dividend payout ratio formula

Mathematicians tend to think of 100% as 1, so they write percentages as decimals.

- 25% would be 0.25

- 75% would be 0.75

If you look at it this way, you can find the dividend payout ratio by subtracting the retention ratio (as a decimal) from 1. Either way, you'll get the same answer.

Dividend payout ratio

Dividend Payout Ratio = 1 - Retention Ratio

How to interpret retained earnings calculations

Do you want high or low retained earnings? That depends on your company's circumstances.

If dividends are rising at a proportionally larger amount each year compared to net income, the retention ratio will decrease. That's an indicator the business is focusing less on growth—because more money is going to shareholders and less is being reinvested.

Startups and smaller, growth-focused companies tend to have high retention ratios. Large companies that are already profitable and comfortable paying dividends will have a lower ratio.

Distributing dividends reduces your retained earnings, whether you pay those dividends in cash or stock. When a company pays dividends in cash, it results in a net reduction in retained earnings.

Can you have negative retained earnings?

Yes, you can. Negative retained earnings may be a reflection of a company's financial performance. It often means that revenue is too low and expenses are too high.

Remember, net income is part of the retained earnings calculation. When that number is negative for a given accounting period, it lowers your company's retained earnings balance—even if that means your ending retained earnings balance is in the red.

However, some companies with long-standing profitability may occasionally report negative retained earnings. This just means the company decided to pay out more than it reported in profits.

So the retained earnings calculation is one indicator of a business's financial health, but it isn't the whole story.

Retained earnings are reported on the balance sheet under shareholders' equity because the retained earnings account represents exactly that—the retained earnings balance that essentially belongs to the company's owners.

Those owners might be stockholders, or they could be private shareholders. It could even be just one or two people for a small, private startup.

As companies grow, their shareholders' equity tends to be split among more and more people or entities—from the venture capital companies that invest in them to, eventually, public stockholders.

Notable considerations about retained earnings

Building up a retained earnings account may sound appealing, but you should keep in mind a few key points about the nature of retained earnings:

- Retained earnings might not provide meaningful insight to investors trying to determine a company's health during a quarter or a year, as they need to compare figures over several years to determine a company's performance.

- Fluctuating profits make retained earnings an uncertain source for investors to gauge a company's performance.

- Some companies underestimate the opportunity cost of building up retained earnings, enabling them to invest in companies or opportunities.

Use automated tracking to process expenses with ease

Retained earnings provide you with important insight into your company's financial strength, but several financial statements need to be prepared to calculate retained earnings.

One of the most important is your company's income statement—and you'll need to process your expenses to put this statement together.

The easiest way to see your company's financial position is to track your operational activities in one place with an expense management platform.

BILL Spend & Expense simplifies the invoice-capturing process by doing all the hard work for you—and it even syncs with most popular business accounting systems. All you have to do is review and approve.

Learn how BILL's expense management software can help you organize your financial data and save time by signing up today or requesting a demo.