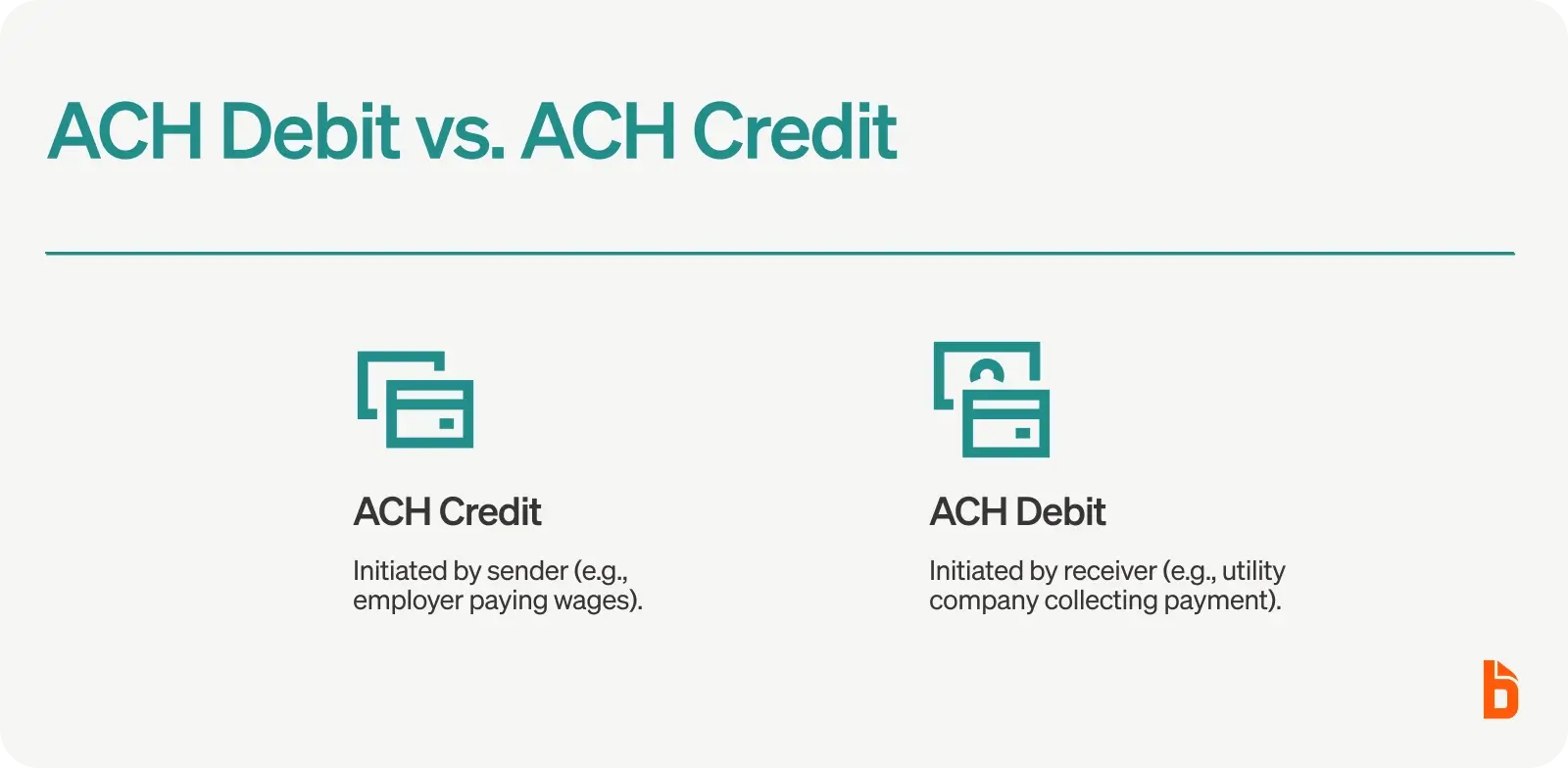

Automated clearing house (ACH) payments can be either ACH debits or ACH credits–– but you won't see those terms used very often. An ACH credit is "pushed" from one account to another. In other words, it's initiated by the party making the payment.

An ACH debit transaction, on the other hand, is "pulled" by the bank account that's being paid. That is, an ACH debit is initiated by the payee—the party that will receive the funding.

This article walks through the various types of ACH debits, the most common related terms, and the benefits of using both ACH debits and ACH credits for your business.

ACH debit meaning

ACH debits are electronic payments made through the ACH network (Automated Clearing House network).

Governed and operated by the National Automated Clearing House Association (NACHA) and including the Federal Reserve, the ACH network is a secure, trusted way to make direct payments from one financial institution to another, transferring funds electronically between accounts.

Payments require prior authorization and are processed in batches automatically. An ACH transaction usually takes 2-5 business days to clear, but same-day ACH payments are also available, clearing in just a few hours.

How does ACH debit work?

When you make an ACH debit payment, you grant the payee permission to withdraw funds from your account. Payers will supply their banking details (bank account number, routing details, etc.) and then authorize the payment with a written contract.

ACH debit payments are often called "pulls" since the recipient actively withdraws funds from the payer's bank account. This also distinguishes ACH debit payments from ACH credit payments—the former involves making payments while the latter involves receiving them.

ACH debit overview

The ACH electronic debit process works like this:

- The recipient provides the details of the transaction to the Originating Depository Financial Institution (ODFI). Details will include the payer's account details, the payment amount, and the due date.

- The processing partner forwards the ACH payment request to the ACH network.

- The ACH network organizes payment requests into individual transactions, then rebundles them to quickly send them to Receiving Depository Financial Institutions (RDFIs).

- The RDFI receives ACH requests and executes transactions. Both the ODFI and RDFI settle transactions with the corresponding Fed balance, though they can also return transactions if they receive an error code.

- The ODFI releases funds to the ACH debit transaction recipient and settles the transaction.

The ACH network submits transactions at 6 am, 12 pm, 4 pm, 5:30 pm, and 10 pm Eastern Time.

Is ACH debit related to debit cards?

ACH debits aren't related to debit cards in any way. Even though both credit and debit card transactions are electronic, ACH debits are used explicitly for bank account transfers. They're actually closer to paper checks in that regard, offering another form of payment distinct from credit/debit transactions.

How long does ACH debit take?

The process to complete ACH transactions takes one to three business days, though the exact time can vary based on the receiving bank. Senders can correct accidental payments with an ACH debit reversal.

What are the different types of ACH debit?

Because an ACH debit is initiated by the payee and pulls funds into their own account, consumer businesses often use it to collect money they're owed. Companies often use terms like "autopay" or "ACH" rather than "ACH debit."

Unique Standard Entry Class (SEC) codes are used to identify ACH debit transactions by type. Here are a few of the most common ones, as examples:

- ARC (Accounts Receivable Entries): a consumer-to-business ACH debit used for converting a source document (like a check) received by mail, at a lockbox, or in person for the payment of a bill.

- BOC (Back Office Conversion): a consumer-to-business ACH debit based on an eligible source document (again, like a check) that a consumer provides at the point of purchase or at a manned bill payment location, later converted to ACH during back office conversion.

- CCD (Corporate Credit or Debit): A single or recurring business-to-business ACH credit or debit payment.

- POP (Point of Purchase): A single business-to-business or business-to-consumer ACH debit based on an eligible source document provided at a point-of-purchase or manned bill payment location.

- POS (Point of Sale): A consumer ACH transaction initiated at an electronic terminal using a merchant-issued physical card or other access device.

Customers have to provide their information, including routing and bank account numbers, and agree to be billed via ACH debit. They're willing to provide that authorization because they see it as a secure service that lets them pay automatically, usually via transfers from their checking or savings account, without needing credit cards or risking late fees.

The benefits to a business are obvious. They can charge customers and receive recurring payments directly from their bank accounts without waiting for the sender. Funds are debited and credited automatically and deposited in their account through timely payments of electronic funds. Companies can protect their income while reducing the potential expense of collecting late or missed payments.

Examples of ACH debit

Examples of ACH debits can include:

- Recurring payments for utility providers or vendors

- Monthly payments on a mortgage or auto loan

- Credit card auto-payments

- Quarterly payments on an insurance policy

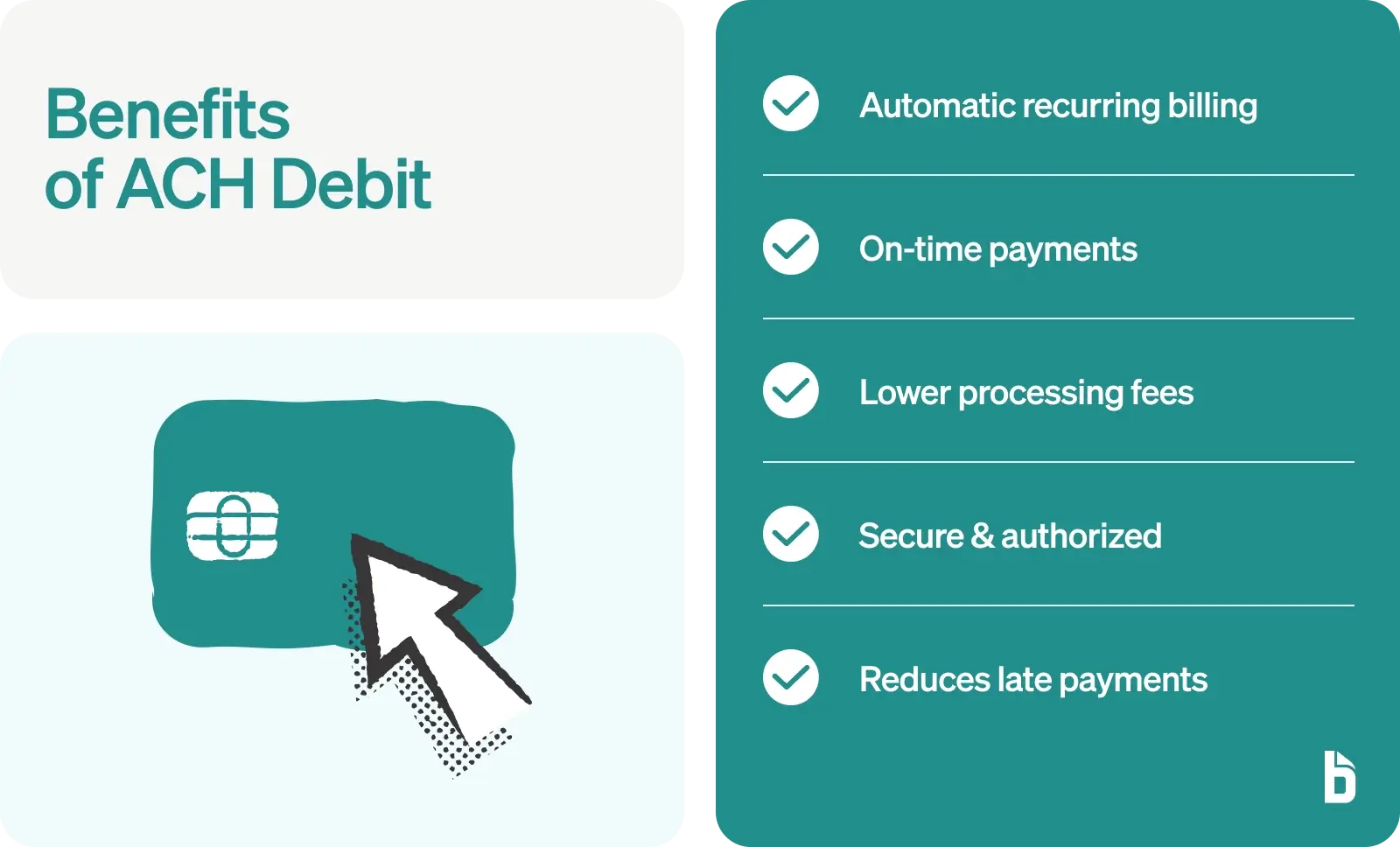

Benefits of ACH Debit

ACH debits are ideal for recurring bills when you know what you can expect to pay and when.

Customers benefit from ACH debits because they can "set it and forget it"—making sure they always pay those bills on time without having to remember them or even lift a finger.

Businesses benefit from ACH debit transactions by getting paid on time, automatically, like clockwork.

Who uses ACH debits?

Anyone can make ACH debits as long as their bank accounts allow this transaction type. ACH debits are common among small business owners, especially for paying recurring invoices or bills such as utility payments. Consumers can also use apps to facilitate a form of ACH payment between users.

If you're a business owner, you can make business-to-business ACH debits. Just make sure your business bank account permits ACH debits—not all banks will conduct these transactions, so you'll either need to find a bank that does or seek an alternative form of payment. You can also institute an ACH debit block to prevent unauthorized payments.

Fees for ACH debit transactions

The cost of an ACH debit can differ by provider. Some banks and providers will allow you to conduct ACH transactions (debits and credits) for no additional fees. Otherwise, you may pay varying rates for the service. ACH fees can be as low as $0.29 or as high as $10.00.

In addition to this flat fee, users may also pay the following:

- Transaction percentage fees

- Monthly fees

- Batch fees

- ACH return fees

Again, these fees vary between providers, and certain ones may not even apply to some ACH debits. Check with your provider to determine your financial obligations and fees.

ACH debit vs. eCheck: What is the difference?

Technically an eCheck is the same thing as an ACH debit, but the term is often used loosely. Almost any electronic funds transfer might be called an "eCheck" no matter who's sending or receiving it. For example, electronic transfers can be batched through the ACH system but can also be sent by wire transfer.

The original meaning of "eCheck," short for "electronic check," has changed over time, so don't assume someone specifically means an ACH debit when they're talking about an "eCheck."

ACH debit vs. direct deposit: What is the difference?

"Direct deposit" is another term for an ACH credit. In contrast to the examples of ACH debits listed above, ACH credits or direct deposits are initiated by the payment source.

They're often used by the U.S. government for both one-time and monthly recurring payments, such as tax refunds and social security payments.

In addition, direct deposit is used by companies to pay workers, merchants, marketing agencies, and more as a matter of convenience.

An employer can deposit paychecks directly into its employee's personal checking account without issuing a paper check. It might also pay for a purchase of goods or services the same way. These payments are fast, simple, easy, and inexpensive, with very low transaction fees, moving between checking accounts without the need for paper.

Why use BILL for ACH payments?

ACH payments can save your business both time and money, and they're more secure than paper checks. But choosing BILL as your intelligent bill pay solution has many advantages.

BILL benefits beyond ACH services include:

- Several convenient payment methods from the same friendly, easy-to-use dashboard.

- Pay by virtual card, ACH, or international wire with just a few clicks.

- Pay by paper check when needed, and BILL will print and mail it for you.

- No matter how you pay, your organization's banking info is always hidden.

- When you want to connect to a vendor for ACH payments, the initial verification process is handled separately on each side.

- Easy lookup for billing statements and payment status.

- Request approvals

- Set up operating rules for automated payments to streamline your AP systems while maintaining corporate compliance guidelines.

Set up ACH payments in BILL today with our risk-free trial.