AP & AR

Overview

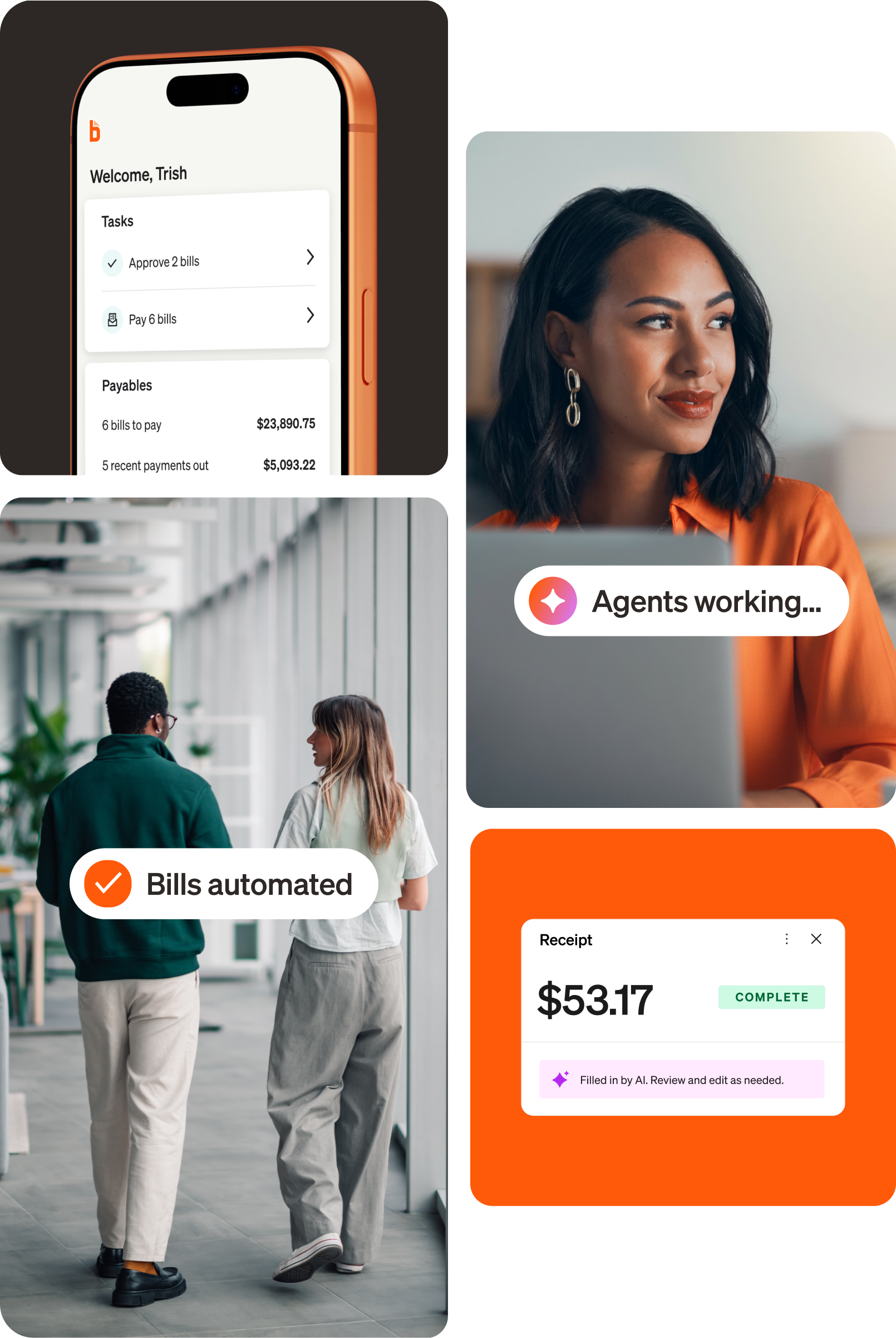

Accounts Payable

Accounts Receivable

Cash Flow Forecasting

Integrations

Features

Pay By Card

ACH Payments

Int'l Payments

Approvals

Invoicing

Procurement

AP Controls

Security

AI

API

Explore BILL's Integrated Platform

Support

Streamline how you pay and get paid

Request a Demo

Spend & Expense

Overview

Spend & Expense

Business Credit

Virtual Card

Integrations

Features

Expenses

Budgets

Mobile App

Reporting & Insights

Rewards

Reimbursements

Payments Services

AI

API

Explore BILL's Integrated Platform

Support

Get credit, control budgets, and manage spend.

Request a Demo

Accounting Firms

Overview

BILL for Accounting Firms

Maximize efficiency and accelerate growth

BILL for Wealth Management

Manage high-net worth clients with confidence

Accountant Resource Center

Tips, tools, and training for accountants

Learn & Connect

Accountant Console

Accountant Partner Program

Pricing for Accountants

Accountant Community Login

Request a Demo

How AI from BILL helps you bypass busy work

Read More

Solutions

Overview

Small Businesses

Easily manage & automate your processes

Midsize Companies

Scale your financial operations efficiently

BILL for Suppliers

Automate incoming payments & cash application

Multi-Entity

Automate for multiple entities or locations

By Industry

Construction

Nonprofits

Education

Professional Services

Healthcare

Retail and Ecommerce

Hospitality

Software and Technology

Manufacturing

Wealth Management

Millions of businesses and accounting firms trust BILL.

Explore Customer Stories

Resources

Overview

Resource Center

Guides, events, and downloadables from BILL

BILL Blog

The #1 blog on all things financial operations

Customer Stories

See how BILL helps thousands of businesses

Learn & Connect

Learning Center

Guides

Webinars

Business Templates

BILL Product Updates

Find an Accountant

Turn bill pay into a scalable white-glove service

Get the Guide

Company

Overview

Press Releases

Official communications from BILL

Investor Relations

Information and resources for investors

Careers

We're Hiring!

Careers overview and current job openings

Partnerships

Explore BILL's partnership opportunities

About BILL

Our Story

Leadership

Newsroom

Contact Us

BILL is making the financial back office a better place

Start Using BILL Today

Pricing

Login

Get Started

Home

/

The Insight Hub

/

Webinars

Webinars

Register Now

Featured On Demand

Accounting

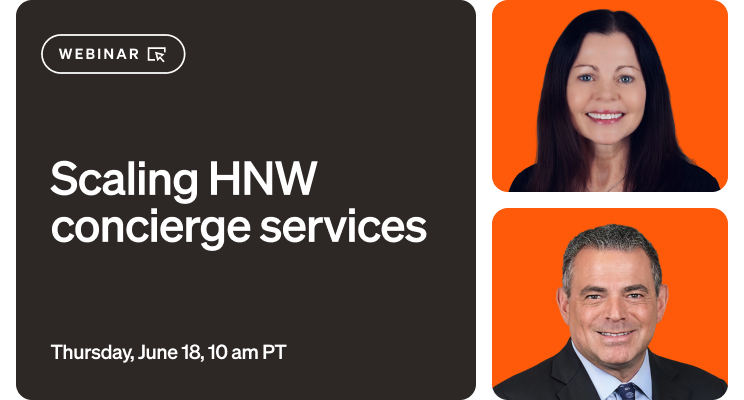

The EisnerAmper standard: Scaling HNW concierge services

Join EisnerAmper for an in-depth session on transforming fragmented bill pay into a standardized growth engine.

Learn More

Business Basics

The silent killers of ((cash flow))

Business Basics

Contractor onboarding in 2026: What finance and HR teams need to know

Accounts Payable

How to future-proof financial operations for growth

Upcoming Webinars

Every Tuesday | 10:00 AM - 11:00 AM PT

BILL basics: The 4 steps of BILL AP

On Demand

Accounting

The EisnerAmper standard: Scaling HNW concierge services

Spend Management

Introducing BILL Travel

BILL

From promises to proof: New findings on the power of AI in finance

Accounts Payable

How to future-proof financial operations for growth

Spend Management

Don't let seasonality slow you down: How to keep cash flow consistent

Business Basics

Nonprofit money & mission: Clarity when it counts

Integrations

How a modern ERP + AP automation can unleash growth

Accounts Receivable

AR benchmarking survey: Why 93% of finance leaders are prioritizing efficiency

Load More