Accounts payable feels like an inevitable part of doing business these days.

For some, managing outstanding invoices has become muscle memory and nothing gets paid late.

But don’t feel bad if something has slipped through the cracks before, a survey of SMBs found that just 13% of respondents reported getting paid on time.

Staying on top of payments, avoiding late fees, and getting in your supplier’s good books all start with better organization.

And better organization can come from an accounts payable ledger.

What is an accounts payable ledger?

The accounts payable ledger is a record of all transactions with vendors that are on credit.

It’s a way to track purchases, payments, and any changes to the liability.

Ledgers have been used since ancient Mesopotamia to keep a clear log of transactions in certain areas of the business.

While a general ledger contains a list of every transaction, an accounts payable ledger is a subledger used to stay on top of liabilities with suppliers.

Who uses an accounts payable ledger?

An accounts payable ledger is most likely to be used by businesses using the accrual accounting method.

This is because it’s a requirement of accrual accounting to record expenses when they are incurred, like when an invoice is received.

However, you can still benefit from an accounts payable ledger if you use the cash basis method.

While it’s not necessary as part of their reporting, having insights into any outstanding liabilities is always beneficial.

Accounts payable ledger entry examples

An accounts payable ledger is typically going to have two types of transactions: purchases and payments.

This means recording a transaction when an invoice is received and when an invoice is paid.

Every transaction you record should contain the same basic information:

- Date

- Amount

- Accounts

You can also add a description like an invoice number to help you understand the ledger at a glance.

Transactions recorded in the accounts payable ledger are double-entry transactions.

Each transaction has two accounts it’s attached to: one is credited and the other is debited.

For now, think of credits as where the money is coming from and debits as where it’s going.

For every transaction, and the ledger as a whole, the debits and credits must be equal.

When someone talks about “balancing the books,” they’re referring to reviewing the transactions to make sure the debits and credits are equal, or “balanced.”

In your accounts payable ledger, one account involved in the transaction will always be accounts payable.

To illustrate this, let’s look at the two main types of transactions that will be in an accounts payable ledger.

Purchase entries

When you initiate a purchase, you receive the invoice that outlines what was purchased, when it was purchased, and the total amount owed.

Let’s say you ordered $10,000 of inventory.

The purchase was made and the invoice was received on June 15th with payment due July 1st.

The purchase entry is recorded on when the invoice was created: June 15th. It will look something like this:

This transaction shows that $10,000 was “taken from” the accounts payable account (and owed to the supplier) for the purchase inventory on June 15th.

The account that’s debited depends on what was purchased.

For example, if you instead purchased new manufacturing equipment, the account being debited would likely be Property, Plant, and Equipment (PP&E).

As a result of this transaction, the accounts payable balance increases by $10,000, which needs to be paid back to the supplier.

Payment entry

On July 1st, you pay your supplier the $10,000 for the inventory purchase by check.

It’s time to update the accounts payable ledger.

For the purchase, accounts payable was credited with the debit reflecting what was purchased.

For payment, accounts payable is debited with the credit reflecting where the money came from.

The credit from the purchase and debit from the payment effectively cancel each other out and reduce the account to zero.

The transaction for a payment looks like this:

The second account being credited in the transaction reflects the invoice payment method.

Since you paid the invoice by check, the funds are taken directly from the bank account and it’s credited.

Say you paid by credit card, that would be the account that’s credited.

The $10,000 that was credited to accounts payable in the purchase entry is offset by the $10,000 that’s debited in the payment entry.

As a result, the accounts payable balance is reduced to $0.

Together, the purchase and payment transactions look like this:

Benefits of an accounts payable ledger

For businesses of all sizes and industries, if you deal with invoices an accounts payable ledger has its benefits.

Insight into your liabilities

The accounts payable ledger acts as the master report of everything accounts payable.

From a glance, you can easily check what your accounts payable balance is and why it’s that amount.

If you aren’t using an accounts payable ledger, you’re digging through transaction histories trying to match payments to invoices.

When comparing information across multiple sources, it’s more likely something gets misrecorded leading to duplicate or missing payments.

It’s also useful for understanding your invoice turnaround times; you can quickly check when an invoice was received and when it was paid.

This is helpful when trying to understand your cash flow and why you might find yourself in a cash crunch after paying down your bills.

Improved vendor relations

Your business cares about invoice turnaround times and ensuring payments are made, but your vendors care even more.

Regularly checking your accounts payable ledger helps you stay on top of your outstanding amounts so you’re never missing an invoice payment.

Missing or late payments sour your relationships with your vendors and could come with interest or late fees.

But if you’re staying up-to-date or even making early payments, you get into the good books of your vendors.

This might open up the possibility of early payment discounts or room for negotiation down the line.

Better understanding of your financial health

Your accounts payable balance is an essential metric to track.

But as with every metric, there’s a nuance behind the number that needs to be understood.

Reviewing your accounts payable ledger gives you the detailed story behind your accounts payable balance.

From that understanding, you can start making changes that improve your accounts payable process.

If your balance is higher than expected, look into the usual invoicing and payment dates.

There might be an opportunity to move billing and payment dates so you’re paying the balance down before another invoice comes in.

In short, if you’re experiencing difficulties paying down your accounts payable, you need to know how your accounts payable cycle works to diagnose the cause.

You can’t get this insight without a clear ledger of transactions to look at.

Common accounts payable ledger mistakes and how to avoid them

Once you’ve decided to use an accounts payable ledger, it’s important to use it correctly.

To start, make sure to avoid these common mistakes.

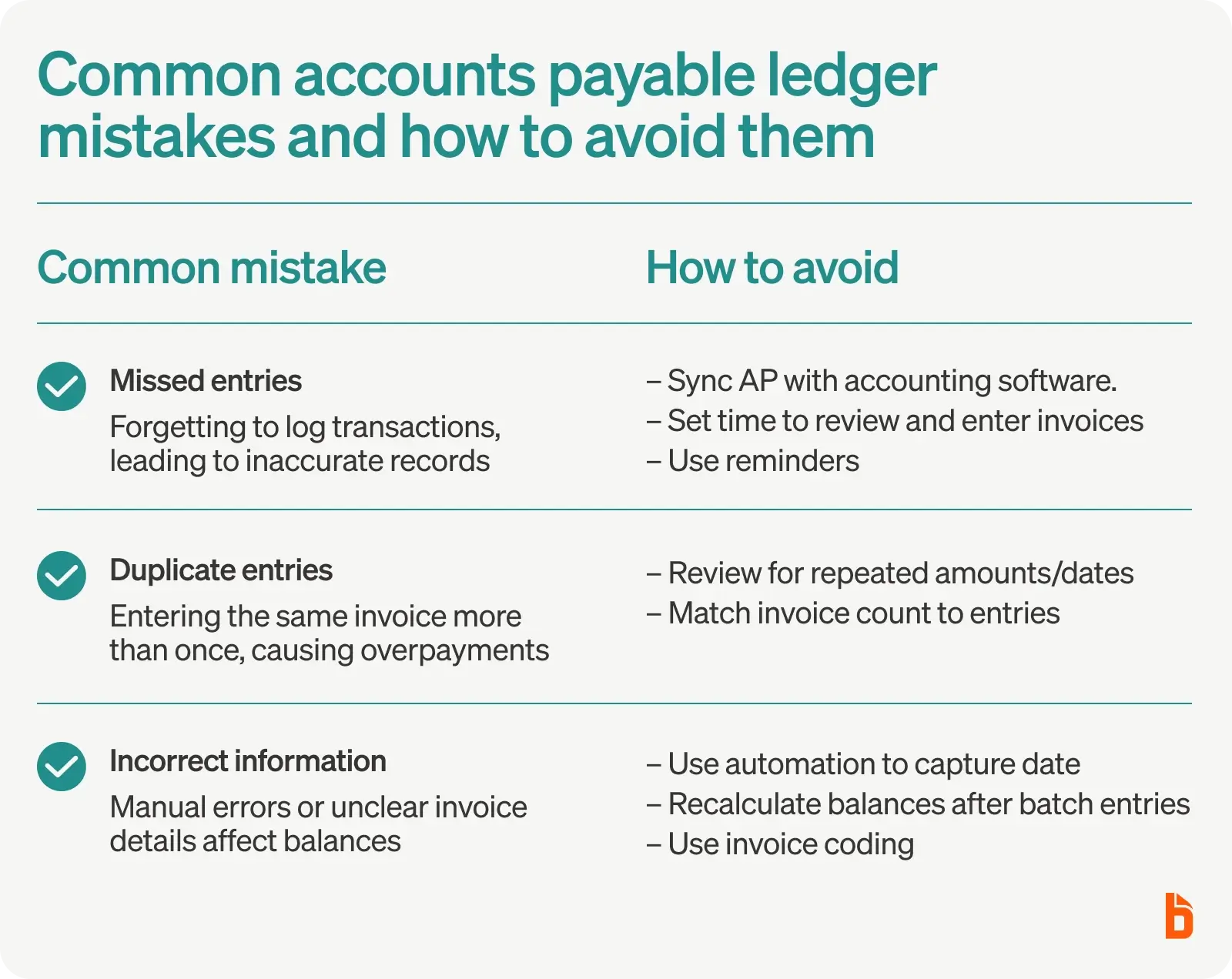

Missed entries

If you’re going to use an accounts payable ledger, make a habit of entering transactions as soon as they happen.

The ledger is intended to be a clear, complete history of transactions and missing an entry causes a ripple effect of problems.

Avoid this by:

- Syncing your accounts payable and accounting software (hint: you can do this will BILL)

- Setting time aside once per day or week to enter invoices and review the accounts payable ledger for accuracy

- Using scheduled reminders to enter an invoice if you can’t enter it as soon as it’s received

Duplicate entries

Duplicate entries are one of the easiest mistakes you can make in an accounts payable ledger.

Sometimes it’s a case of multiple people entering the same invoice.

In other cases, it’s that uncertainty of whether the invoice has been entered yet or not.

The consequences are an inaccurate accounts payable amount, feeling more in debt than you are, and duplicate payments.

As much as your suppliers would love being paid twice, it’s an easily avoidable mistake if you spend some extra time reviewing your entries.

Avoid this by:

- Looking for repeated amounts on the same date in the ledger

- Counting up the amount of transactions you entered and confirming it matches the amount of invoices entered

Incorrectly entered information

Human error is always a possibility with a manual process.

All it takes is one finger slightly missing the mark on a keyboard and the balance is off.

There can also be ambiguity in what account was used to pay the invoice or what expense type the invoice was.

These types of mistakes impact your accounting down the line as account balances will be off and expenses inaccurate.

Avoid this by:

- Using automation (with BILL) to automatically validate and capture invoice data

- Calculating what your accounts payable balance should be after entering a batch of invoices so if the balance doesn’t match, you know something is wrong

- Use invoice coding to get rid of any ambiguity on an invoice

Better accounts payable with BILL

A good accounts payable team will use an accounts payable ledger to stay on top of their invoices.

A great accounts payable team uses tech to cut down on errors, reduce processing times, and run an efficient operation.

Using BILL, your accounts payable team has all the information they need to excel at their work.

Customized workflows keeps the accounts payable process running smoothly while in-platform payment options makes sending money as easy as clicking a button.

Pair that with a dashboard that makes tracking essential metrics a breeze and your accounts payable system gets ramped up to the next level.

Try BILL to see for yourself how we save businesses 50% of their time spent on accounts payable.