One of the first decisions you need to make when you start a business is deciding whether you’ll use the cash basis accounting method or accrual basis accounting. This is a major decision that shapes how you account for income and expenses and pay taxes.

Cash basis accounting is usually a good fit for small businesses that don’t carry a lot of inventory because it’s simple and easy to use without a lot of accounting knowledge.

However, you might need to eventually switch to accrual accounting if your business grows past a certain point or you want financial reports that better represent your business operations. Here, we’ll cover everything you need to know about the basics of cash basis accounting.

What is cash basis accounting?

Cash basis accounting is an accounting system in which you record revenue or expenses when cash is received or paid. This means that you record income when a customer hands you cash, a check, or digital payment. In commerce, “cash” refers to any money you receive, even if it’s not in the form of physical currency.

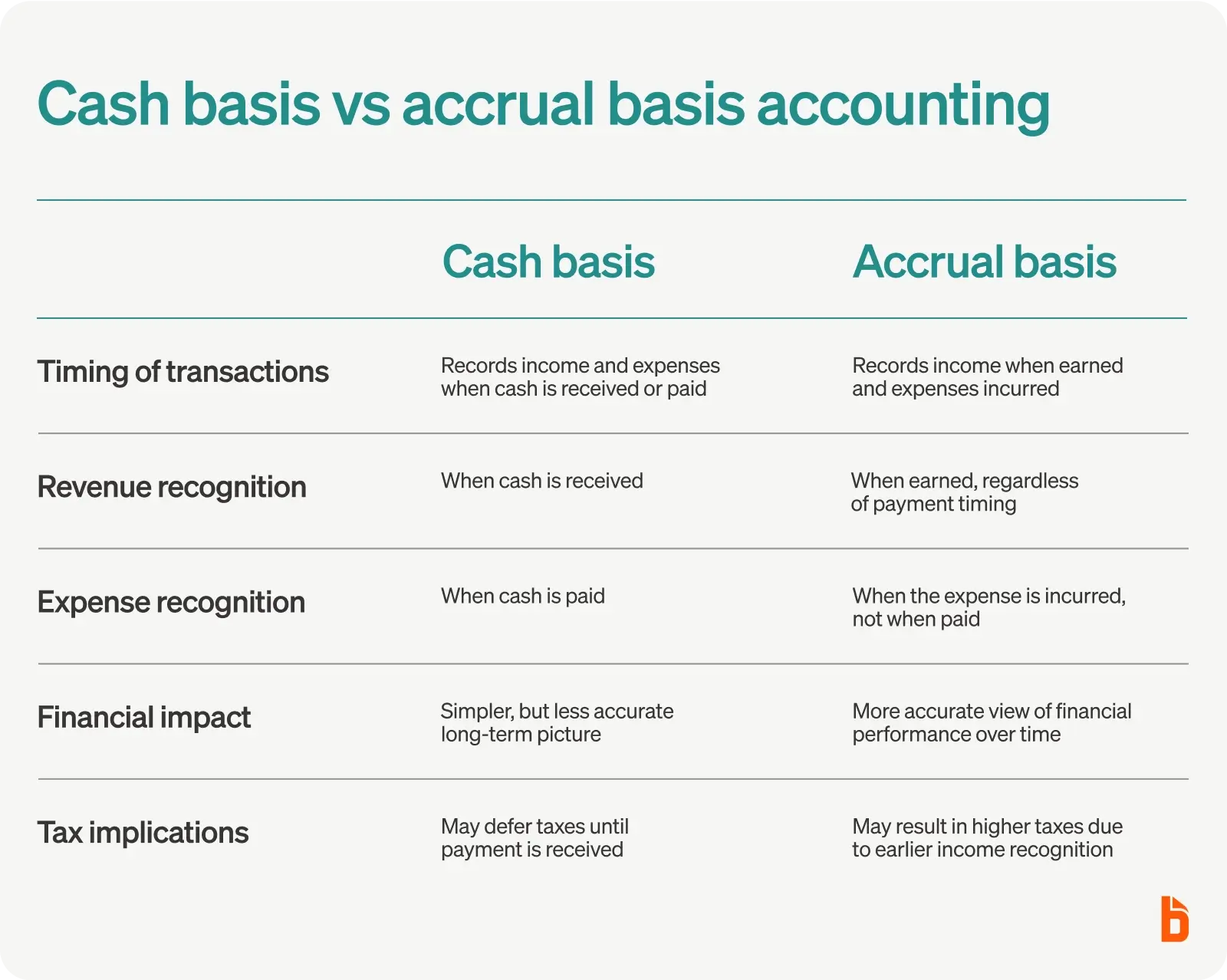

Cash basis vs. accrual basis accounting

Cash and accrual accounting are two different accounting methods, so it’s good to know how each operates as you decide how to account for your business transactions.

The difference between cash and accrual basis accounting essentially all comes down to the timing of recording transactions:

- Cash basis accounting recognizes revenues when your business receives cash or pays expenses—in other words, when cash changes hands.

- Accrual accounting recognizes revenues when earned and expenses when incurred, regardless of when cash actually changes hands..

The timing of these transactions affects how you prepare financial statements and how much tax you owe every year.

Financial statements in cash basis accounting

No matter your industry or the size of your company, you generally have the same three foundational financial statements: the income statement, balance sheet, and cash flow statement. Here’s how cash basis accounting affects each of these statements.

- Income statement: A cash basis income statement only includes revenue and expenses you actually received or paid during the accounting period. So cash basis net income reflects cash received and disbursed over the month, quarter, or year rather than the total revenue earned (but not received) and expenses incurred (but not yet paid).

- Balance sheet: A cash basis balance sheet does not include certain assets and liabilities. For example, it doesn’t include accounts payable or accounts receivable.

- Cash flow statement: It’s usually easier to prepare a cash flow statement using cash basis accounting because you don’t have to adjust for items that don’t affect cash, like accounts payable, accounts receivable, and accrued expenses.

Cash basis accounting example

Let’s take an example to get a clear picture of how cash basis accounting works:

Say you have a project to complete between April 1st and May 30th valued at $10,000. Your client pays a 50% deposit, and you agree to have half of the project deliverables ready on April 30th, with the remaining deliverables to the client by May 30th. At that point, you’ll send an invoice for the remaining contract fee.

- If you use the accrual method of accounting, you record $5,000 of revenue when you provide the first set of deliverables on April 30th and another $5,000 of revenue when you complete the work. It doesn’t matter when the client actually pays the invoices

- With the cash method, you record the first $5,000 as revenue when the client gives you their 50% deposit. You would recognize the other $5,000 of revenue when the client pays the invoice sometime after May 30th.

Why your business might use cash basis accounting

Many small businesses, community associations, non-profit organizations, and other entities use the cash method because of its simplicity: Cash basis accounting is straightforward, and it makes preparing financial statements and tax returns easy for business owners.

You might opt for cash basis accounting if:

- You don’t have to issue financial statements that follow generally accepted accounting principles (GAAP). GAAP requires companies to use accrual accounting.

- You have under $30 million in average gross receipts over the past three years. The IRS requires businesses with average gross receipts above that threshold to use the accrual method.

- Inventory is a big part of your business. Most companies that carry inventory need to use accrual accounting, as it does a better job of allocating expenses to the period in which the corresponding revenue was earned.

Tax breakdown with the cash accounting method

The accounting method you use impact your tax liability. Let’s say your business had the following transactions last month:

- You sent a $5,000 invoice for a project you completed, but the client hasn’t yet paid the invoice.

- You received a bill for $1,000 from a freelance designer you hired. You haven’t yet paid the bill.

- Paid $75 for supplies with your business debit card.

- You received $1,000 for a project you completed the month prior.

If you use the cash method, your net income for this month would be $925. Here’s why:

$1,000 (cash received) – $75 (supplies) = $925 (net income)

Using the accrual method, your net income would be $3,925. That’s the $5,000 of revenue from the completed project, minus the $1,000 due to the freelance designer, minus the $75 you paid for supplies. The $1,000 cash receipt doesn’t factor into this month’s net income because you recognized the income from that project last month.

As you can see, the cash method is beneficial because you don’t have to pay taxes on income you haven’t yet received. It also gives you more leeway for tax planning.

For example, say you want to minimize your taxable income. At year-end, you might put off sending invoices to clients until January to defer revenue until next year and prepay next month’s rent and utilities to accelerate expenses into this tax year. This kind of tax strategizing isn’t possible using accrual accounting.

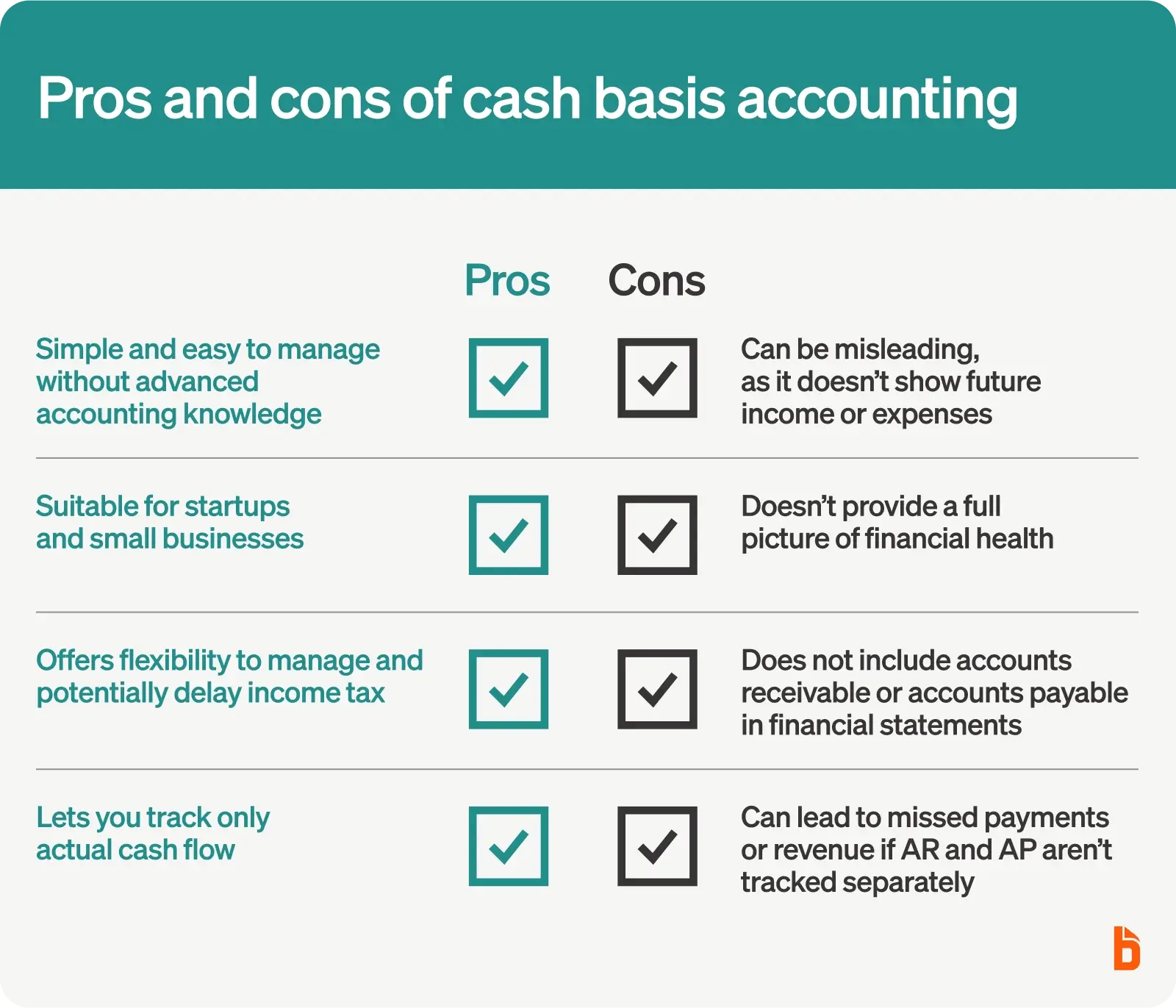

Pros and cons of cash basis accounting

As a business owner, you want to choose the accounting method that’s right for your business. Selecting the wrong accounting method could mean paying more taxes, complicated accounting workflows, and less useful financial statements. It might also mean needing to change your accounting method down the line, which requires applying for a change in accounting method with the IRS and potentially restating your financial statements.

To help you make the right choice now, here are a few pros and cons of cash basis accounting:

Benefits of cash basis accounting

1. Cash basis accounting is a simple, straightforward process

As a business owner, all you have to do is track money as it moves in and out of your business bank account. You don’t have to factor in expenses you haven’t paid for yet or payments you haven’t yet received.

Because the cash basis method is easy to understand, business owners without a lot of accounting knowledge can manage their bookkeeping without hiring an accountant — which is why it’s such a popular option for startups and small companies.

2. Cash basis accounting offers manageable income tax

Because you only record the money going in and out of your business account, you have more control over your tax liability. If you send an invoice of $2,000 to a client in November and they pay you in January of next year, you won’t pay tax for that transaction until the following year.

This method might help you delay paying income tax on earnings until you collect the money — which can be especially helpful for small businesses with tight cash flow. You can also lower your tax burden by pre-paying business expenses in November or December, even though you won’t use those services until the following year.

Drawbacks of cash basis accounting

1. The cash basis method could be misleading

Cash basis accounting only shows you how much cash you’ve brought in or paid out. It doesn’t reflect any planned transactions. As such, it’s challenging to get a long-term picture of financial health. For example, it might appear that the company has a lot of cash in the bank and positive net revenue, even though it owes thousands of dollars to its suppliers. This aspect of cash accounting can be misleading to investors and lenders.

2. Cash basis of accounting does not record accounts receivable and accounts payable

Accrual accounting includes accounts receivable (A/R) and accounts payable (A/P) in financial statements, which inform you of what payments you will receive and your outstanding bills.

Without these items in your statements, you might have difficulty keeping track of what you are owed and what you owe.

Not having this vital information could damage your finances. For example, you might forget a client owes you money for work you already performed.

Automatically track your budget and expenses with the right tools

Cash and accrual accounting are two ways businesses can track their financial performance. The cash basis system is usually used in small business accounting because of its simplicity and ease, while the accrual basis system provides a more accurate picture of your business performance.

Whichever accounting method you choose for your business, tracking your spending is the first step to understanding business finances and cash flow patterns. BILL Spend & Expense can help you take control of your budget and start spending smarter with customizable spending controls and policies. Schedule a personalized BILL Spend & Expense demo to learn more about what it can do for your company’s financial health.