Gone are the days of needing to hand over cash and paper checks to make and receive payments. As the scope of business expands beyond state lines, digital payments are increasingly becoming the norm for getting money into the hands of recipients.

Commonly used for both single and recurring transactions, ACH payments make it easy to send money from one bank account to another without the need for a paper check.

Here, we’ll cover what exactly an ACH payment is, how it works, and how it compares to other common payment methods available to businesses.

What is an ACH payment?

An ACH payment is a payment sent via the ACH (Automated Clearing House) network (also called the ACH payment system), an electronic network used to send paperless payments between bank accounts in the United States.

If you think of payments as the money taken out of your account when you have your monthly bills on autopay - that’s typically done via ACH. Deposits are a category that includes your paycheck coming via direct deposit.

Established in the 1970s to deal with the growing number of paper checks needing processing, the ACH network now processes an enormous volume of direct payments more safely and efficiently than paper checks. According to PaymentsJournal, in 2022, the ACH Network safely processed 30 billion payments valued at over $76 trillion.

You may also hear ACH payments referred to as e-checks because it was intended to be a substitute for the less efficient paper check. Now it’s one of the most common forms of electronic payment, processing over 33 billion transactions in 2024 alone.

What is NACHA?

NACHA stands for the National Automated Clearing House Association, a non-profit association that is responsible for managing the rules and standards of how direct payments move through the ACH network.

They also develop tools and educational materials that make ACH payments more accessible for businesses and individuals alike.

As a non-profit, its funding comes from the financial institutions that make use of the ACH network.

The oversight and governance that NACHA provides help maintain the safety and reliability of ACH payments.

How do ACH payments work?

When a payer authorizes a payment, the bank submits the details to the ACH network, which routes the transaction to the recipient's bank. The recipient's bank then credits the payee's checking account while debiting the payer's account—a process known as settlement.

Perhaps the most well-known example of an ACH transaction is payroll direct deposit. This is a good scenario to explain how the ACH network works since many Americans receive their paychecks that way:

- Employee enters their bank number into the payroll system.

- Employer initiates payment several days before payday to ensure payments arrive on time.

- ACH payment is batched, processed, and routed to the correct banks.

- Payment is deposited into the employee's account.

Typically, funds show up in the receiving depository financial institution in 1-3 business days—a process much faster than paper checks. Financial institutions can also choose to have ACH credits processed and delivered within one business day, per guidelines set forth by NACHA. Those same guidelines state that ACH debits must be processed by the next business day. With an increasing need for faster transaction times, most major banks and credit unions are on this system.

What are the types of ACH payments?

There are two types of ACH payments: credit and debit transactions. The difference between the two transaction types is who is initiating the payment, either the payer or the payee.

An ACH credit is initiated by the payer. Often referred to as a “push” transaction, as the payer is “pushing” the money towards the payee. This is the most similar to writing a check, as it involves the account holder providing the details of the recipient and amount, much like they are filling out the fields on a paper check.

Examples of ACH credits are using direct payment methods for paying taxes, processing payroll, or making vendor payments.

An ACH debit is initiated by the payee. These transactions are called “pull” transactions because the receiving account submits a request to “pull” the funds from the payer’s account.

ACH debits are most commonly used for recurring bills like mortgage payments or utility bills. If the payer has direct deposit set up, the payments are automatically processed without having to manually enter information or initiate the transfer.

You’ll likely use both throughout the course of your operations. ACH credits are most commonly used for one-time payments, while ACH debits are used for recurring payments that can be initiated without the need for approval.

Benefits of using the ACH network

If you’re considering the ACH network for electronic payments, there are several benefits to consider. They include:

- Lower processing fees: ACH transactions fees average out at $0.29. Credit card processing costs, on average, 1.3% to 3.5% of the transaction. Do the math. There’s a significant savings potential with using ACH payments.

- Fewer declined transactions: Credit cards get denied and checks bounce. Insufficient funds can happen when using ACH, but it's less common and the bank is on your side when it comes to collecting the payments that are due.

- Convenience: No need to write checks, deposit them, or even run credit cards.

- Convenience for your customers: Autopay by ACH payment is far from a new concept. Most consumers are already doing it for bill paying. Offering it as a payment option for your business is adding a convenience. Your customers will appreciate you for it.

Limitations of the ACH network

There are a few limitations of the ACH network that all businesses should be aware of:

- Transfer limits: There are same-day maximum transfer limits. If your volume is higher than what’s allowed, this could be a problem.

- Cutoff times: Paper check deposits don’t count until the next day if made after 2:00 PM. ACH transactions are no different.

- International transactions: The ACH network is only available inside the United States, so businesses operating internationally will need another option.

How to set up ACH payments for your business

Once you’ve made the decision to start accepting ACH payments for your business, the setup process is simple. If you’re using a payment solution like BILL, you only need to sign in, connect a bank account, and add customers or vendors. The mechanism to request ACH payments is already built into the software. If you’re doing this manually, here are the steps you need to take:

- Set up an ACH merchant account: You’ll need a federal tax ID number for this. You will be asked how long you’ve been in business and what your estimated volume will be.

- Request customer authorization: When done manually, this requires paper or online forms. You can do it with a phone call, but it’s better to have written documentation.

- Set up payment details: You’ll need bank routing and account numbers from each of your customers, along with payment amounts and frequency.

- Submit payment information: You’ll need payment processing software for this, so it’s probably simpler to just let BILL handle the whole process for you.

ACH payments for recurring bills

The ACH network is often used to pay bills, especially monthly recurring bills. Many vendors prefer this method because the processing cost is lower than credit cards and faster than waiting for paper checks. Examples of the types of bills you may already be paying with ACH payments include:

- Credit card monthly payments

- Utility payments

- Auto loan payments

- Mortgage payments

- Merchandise on monthly payments

Bill payments are usually listed as ACH debits, while payments to your account from another entity, like the US Government or IRS, are classified as ACH credits. The difference is that credits are pushed into an account while debits are pulled out of the account. Hopefully, that alleviates any confusion.

ACH payments involve three other parties in addition to the Automated Clearing House itself. Those three parties are:

- The Originating Depository Financial Institution (ODFI)

- The Receiving Depository Institution (RDFI)

- The National Automated Clearing House Association (NACHA)

The ODFI initiates the transaction and the RDFI receives it and processes it through the Automated Clearing House. NACHA is the governmental agency that oversees and writes the regulations for the ACH. They protect you from fraud and ensure that the network works at optimal speed, so you don’t have to wait weeks for payments to process.

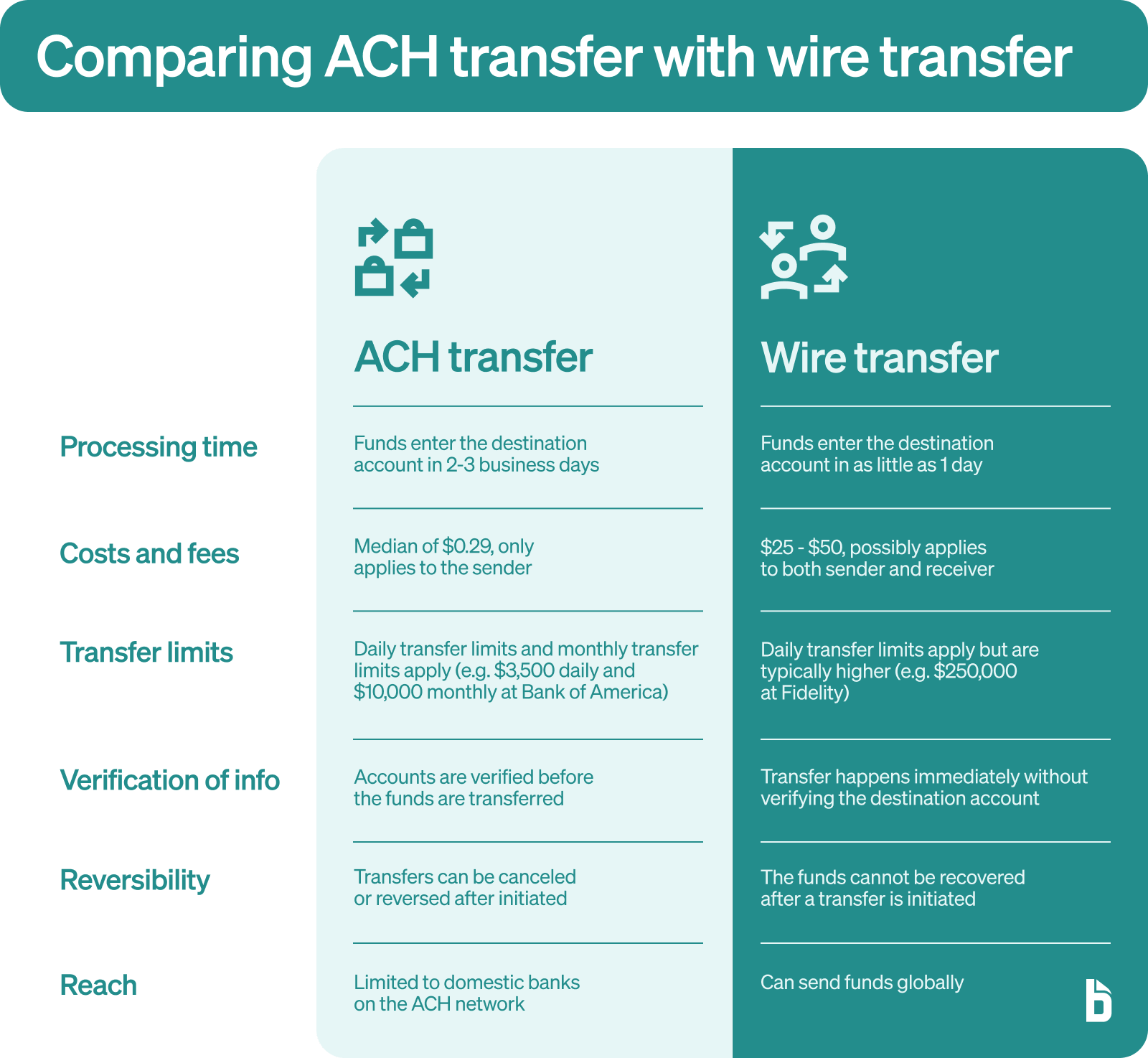

ACH payments vs wire transfers

Both ACH payments and wire transfers are forms of electronic money transfers.

Wire transfers process payments in real time over the Swift Network and can get you your money in a few hours.

ACH transfers use the Automated Clearing House Network and can take several days to process.

Of course, you pay for that convenience. Anyone who’s ever sent money using Western Union knows that the cost is high, sometimes as much as $60, depending on the amount being sent. It’s a nice option to have if someone needs funds quickly, but it’s too expensive for merchants to use as an everyday direct payment method. ACH transfers usually cost under $1.

For a more in-depth comparison, check out this guide: ACH transfer vs. wire transfer: The payment choice is clear and the comparison table below:

ACH payments vs EFT payments

There are some important differences between these payment methods that may help you decide which one is best for your situation.

EFT stands for electronic funds transfer. EFT payments refer to any kind of payment that’s made electronically, including wire transfers and virtual card payments.

ACH payments (and eChecks) are considered one type of EFT payment. While you can use EFT payments to refer to any ACH payments, it’s best to be specific to ensure there’s no miscommunication between you and your customers or suppliers.

Are ACH payments right for your business?

Here are some questions that’ll help you decide whether or not ACH payments are right for your business.

Does your business accept recurring payments?

Subscription services and service providers generally fall into this category.

Customers are able to make their monthly payments with credit cards, but the processing fees for the business can be expensive. ACH transaction fees are more cost effective. The median cost is just $0.29 per transaction.

Are you currently taking paper checks?

Any business owner or manager who does daily reconciliation can tell you that counting checks at the end of the day is time consuming and inefficient.

Handwritten checks are sometimes difficult to read and each one needs to be checked for proper date, amount, signature, and contact info.

Paper checks are an archaic and outdated system. They need to be deposited, and can be stolen or lost in the mail. ACH transactions are faster and more efficient.

Are your customers comfortable with online transactions?

Most people are the days, but if you have an older customer base you may face some resistance. Making the transition to ACH transactions requires commitment from the business owner. It may take some time for customers to fully embrace it.

ACH rejection codes and reasons

Though rejections and denials are a risk with any payment method (except cash), this might be considered another drawback. There are times when a request for an ACH payment or deposit may be rejected. There are several reasons that could happen. If you experience this, look for one of the following rejection codes on the transaction statement:

- R01: Insufficient Funds: This is most often seen when a customer initiates a payment and doesn’t have enough money in their account to cover it. The customer should contact their financial institution right away if this happens to avoid NSF fees.

- R02: Bank Account Closed: When an account has been closed and the payer doesn’t inform the payee, this rejection code will appear on the payee side. The best course of action is to call the customer and get updated account information.

- R03: Unable to Locate Account: This code is often an error on the payee side. It’s possible you were given incorrect information, but you should check your own work before you jump to conclusions.

- R04: Rejection: When the system kicks back a simple R04 “Reject” response, it means that the bank isn't allowing the sender to withdraw funds from that account. Usually, the bank just needs an originator code to enable ACH withdrawals.

Like checks with insufficient funds (NSF), the bank will charge a fee if your business triggers a rejection code. This may have been caused by an inadvertent error on the data entry side or due to an accounting mistake. Either way, contact your bank right away if you get a rejection code. They might be willing to waive the fee if you act promptly.

Frequently asked questions

Is the Automated Clearing House secure?

NACHA has a set of rules and regulations that govern the ACH process and determine eligibility for businesses using the network. Among those mandates is the requirement that businesses and third-party processors encrypt banking information with “commercially reasonable” technology. Today, that means 256-bit SSL encryption. Additional security is provided by the payment processor. Together, these requirements make the ACH process very secure.

What’s the difference between an ACH payment and direct deposit?

Direct deposit is simply a type of ACH payment. In fact, direct deposit is perhaps the most common type of ACH payment, seeing how common it is for employees to receive their paycheck directly in their bank accounts via direct deposit.

How long does it take for an ACH payment to go through?

ACH processing times range from 1-3 business days to complete. ACH payments are not instantaneous, and are processed in batches throughout the day. Depending on a variety of factors, including the bank doing due diligence to ensure sufficient funds are available, the payment may take a few business days to go through.

Some institutions offer same day ACH payments, but charge a fee for same day processing.

Are ACH payments different from credit card payments?

Yes, ACH payments are different than credit card payments.

ACH payments transfer money between bank accounts through the ACH network. There isn’t an intermediary party as the payment is direct between the payer and the payee. The downside is that these funds can take 3-5 business days to be deposited.

Credit card purchases are instant, with funds being charged to the card at the time of the transaction. The business is typically charged a percentage fee for processing the credit card payment. It’s then the cardholder’s responsibility to pay down the balance of all the charges made to the card.

How much does it cost to process an ACH payment?

The cost of an ACH payment depends on the ACH processor. Typically, an ACH fee is a flat cost that ranges from $0.25 to $5.00. Some processors may charge a percentage cost, but that option is only best if you’re processing small transaction amounts.

Compared to other payment methods like credit cards or wire transfers, the cost of ACH payments is often lower for the receiver.