The terms electronic data interchange (EDI), automated clearing house (ACH), and electronic funds transfer (EFT) are sometimes mistakenly used interchangeably.

While these terms might sound similar or even perform similar functions, each one has a distinct definition from the other and has its own legal impact. Here’s what you need to know about the differences between EDI, ACH, and EFT; the types of “EDI payments” you can use; and how they can be used in your business.

What are EDI payments?

Technically, EDI is not a payment format, but you’ll still see the term “EDI payment” fairly often. An “EDI payment” is just a payment that happens to include data that’s in the Electronic Data Interchange (EDI) format. EDI is meant for exchanges of information between computers or other technology devices.

Here are a few types of documents that can be used and managed with EDI:

- Purchase orders

- Invoices

- Bills

- Payment documentation

Many businesses deal with sensitive data. Using paper to track that information can lead to security issues, mistakes due to human error, and much slower communication rates. Electronic data interchange, or EDI, is an electronic format for transmitting data. This alternative is generally considered to be more secure than paper-based methods because it allows for data encryption and tends to be easier to manage than tracking a stack of documents.

According to NACHA, “In the payments world, EDI can be used to format invoice and remittance information.”

In other words, EDI is used to format information that accompanies a payment — such as the number of the invoice being paid.

What’s the difference between EDI, ACH, and EFT?

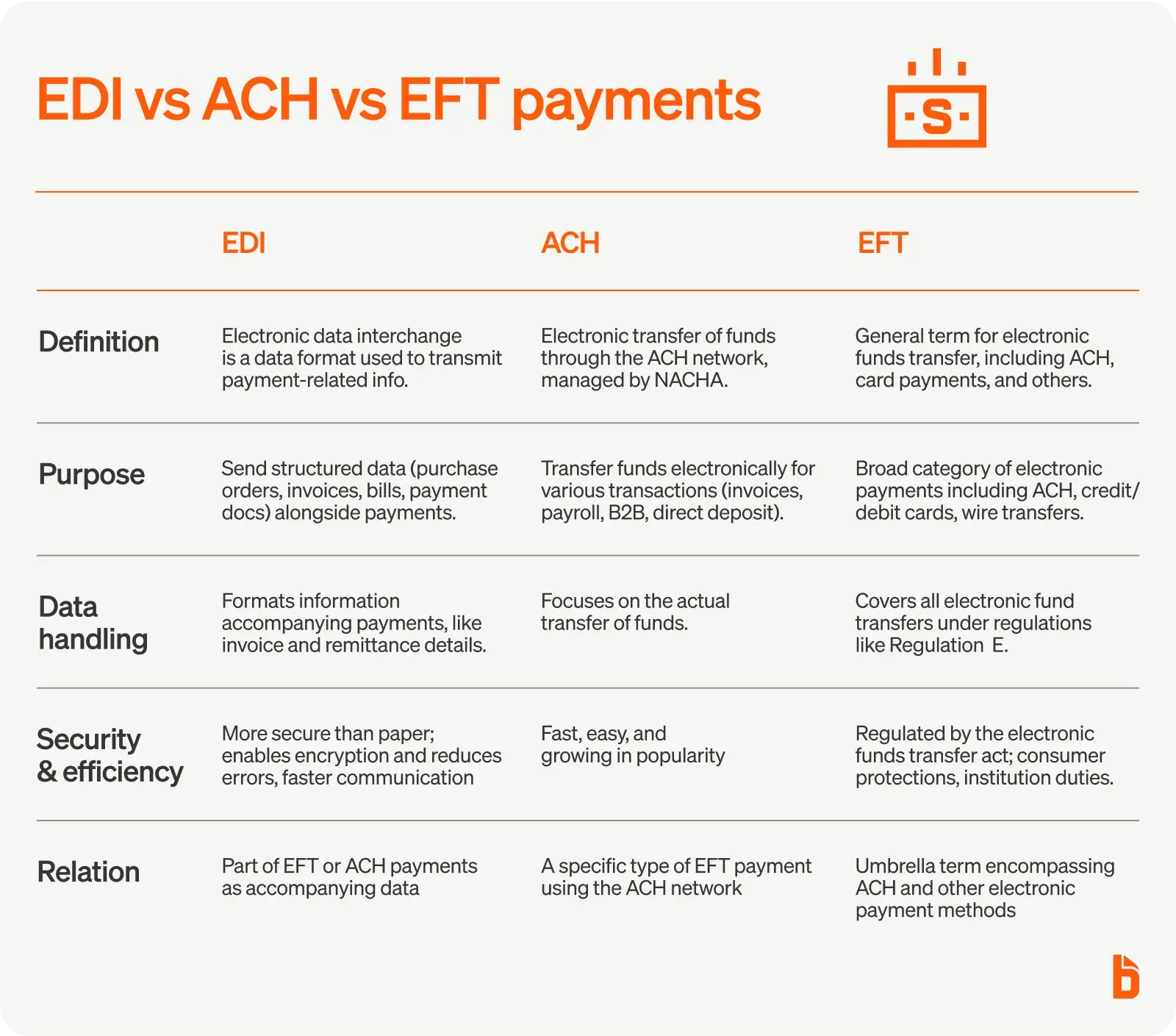

EDI vs. ACH

ACH, or automated clearing house payments, refers to the electronic transfer of funds through the ACH network. This is managed by the National Automated Clearing House Association (NACHA). An ACH payment can be used for just about any kind of payment or money transfer, such as paying invoices, business-to-business (B2B) transactions, direct deposit, and payroll for your employees.

ACH is an extremely common approach to payments, and seems to only be growing in its popularity. According to a 2019 notice by NACHA, the use of ACH transactions had expanded by more than one billion for the previous five years. That same year, there were 24.7 billion ACH payments which totaled $55.8 trillion.

The popularity of ACH may be due to the fact that it can make the payment process extremely fast and easy. The convenience of paying or getting paid quickly can be an attractive option for many businesses.

EDI vs. EFT

EFT, also referred to as electronic funds transfer, is a more general term for electronic payments. An ACH is a particular kind of EFT — specifically, one that uses the ACH network for the payment transfer. But not all EFT payments are ACH payments. There are other kids of EFT payments as well, such as paying online with a credit or debit card.

EFT is also sometimes referred to as Regulation E because of the Electronic Funds Transfer Act. This legislative policy outlines both consumer rights and financial institutions’ responsibilities when it comes to the electronic transfer of funds. The Consumer Financial Protection Bureau regulates this policy.

EDI is not a payment format, but it’s still related to EFT in the same way that it’s related to ACH — because any electronic payment could include additional data that uses the EDI format.

What are the types of EDI payments?

Because additional data can be included in just about any electronic funds transfer (EFT) using the EDI format, the types of “EDI payments” are as varied as the types of EFTs. As a result, the terminology can get a bit confusing — many people use terms like Web EFT and Web EDI interchangeably.

For example:

- Web EDI: As the name implies, this type of EFT payment uses Internet browsers to process payments. Because these payments also include other types of payment information, such as the item being purchased or the invoice being paid, they are often referred to as Web EDI payments — web-based EFT payments that include data in the EDI format.

- Direct EDI/Point-to-Point: More properly called direct EFT, these point-to-point payments require business partners to connect with each other directly for payment. This approach is generally best for larger businesses that deal with many payments and transactions on a daily basis, often with the same business partners Because these payments often include data in the EDI format, they’re sometimes called Direct EDI payments.

How do EDI payments work?

There are two main differences between manual payments and “EDI payments,” no matter which form of EFT is actually used to make the payment.

- The payment itself is transmitted through some sort of EFT instead of using a paper check — ACH and credit cards are two of the most common

- The data that goes with the payment is captured and transmitted electronically, using EDI, instead of using paper

Those two simple differences lead to a whole host of benefits for most businesses.

- The data that accompanies each payment is transmitted electronically, speeding up the entire payment process significantly

- When data is transmitted electronically, it can flow through your ERP or accounting system without any need for manual intervention

- Data is copied automatically from each step to the next, minimizing the chance of human error

- Payments are made more quickly and easily

- Automation software can take advantage of these electronic formats, simplifying your accounting efforts even more — such as letting you set departmental budgets ahead of time via corporate credit cards and automating expense management

What are the benefits of using EDI payments?

Using EDI can have a positive impact on your bottom line as well as the efficiency of your back-office operations. In accounts payable and accounts receivable, for example, EDI and electronic payments can cut back on extraneous paperwork, streamline invoicing and approval systems, and minimize manual accounting tasks.

This time can then be spent on other aspects of your business, including higher-level projects that could make your company more profitable.

EDI and electronic payment systems can also help you cut back on accounting errors because EDI technology can help you minimize the chance of common mistakes brought on by human error. At the same time, these systems can significantly reduce the time it takes to pay employees for out-of-pocket expenses as well as the time it takes to pay critical vendors — improving relationships with both.

The bottom line

When it comes to making or receiving payments for your business, EDI and EFT payments can help streamline your accounting process, making life simpler for everyone involved. When paired with automation solutions, the efficiencies can be even more impressive, freeing up your time while providing more visibility into your company’s finances.