As companies adjust to new ways of working while continuing to pursue higher revenues, finance departments are under increased pressure to handle more payments and invoices in less time, with fewer resources. Staffing shortages and difficulties retaining top talent only make it harder for accounting professionals to keep pace with new demands.

Optimizing your company’s finance functions can save time without overtaxing employees or reducing their capacity for work. Employee turnover and fraud risks will both decline, while agility and growth potential will increase exponentially.

What is the role of a finance function?

Finance functions are vital components of many different financial responsibilities within a business. This umbrella term encompasses financial reporting, budgeting, forecasting, accounts payable, accounts receivable, and ensuring compliance with tax and reporting regulations.

In some cases, finance functions are handled by a robust team of specialists, each handling one part of the process. But for small to medium businesses (SMBs), finance departments are composed of people who wear multiple hats, juggling each responsibility.

No matter the size of the team, the role of the finance function is the same: process, record, monitor, and report on every dollar that enters and leaves the business.

How do finance functions impact business profitability

There are two main ways finance functions impact business profitability.

The first is the administrative costs of completing the financial processes. Inefficient workflows relying on manual inputs struggle to scale as operations grow, forcing the business to invest in additional headcount.

The more that a finance department relies on manual labor, the more costs they’ll face as the business grows. This limits how much additional profit a business pockets from new sales revenue.

The second way finance functions impact business profitability is how they invest their time. If they’re too busy completing administrative tasks, they won’t have time for high–value work like cost-benefit analysis, budgeting, and forecasting.

Both of these dynamics can be improved with investments in streamlining and automating your finance department.

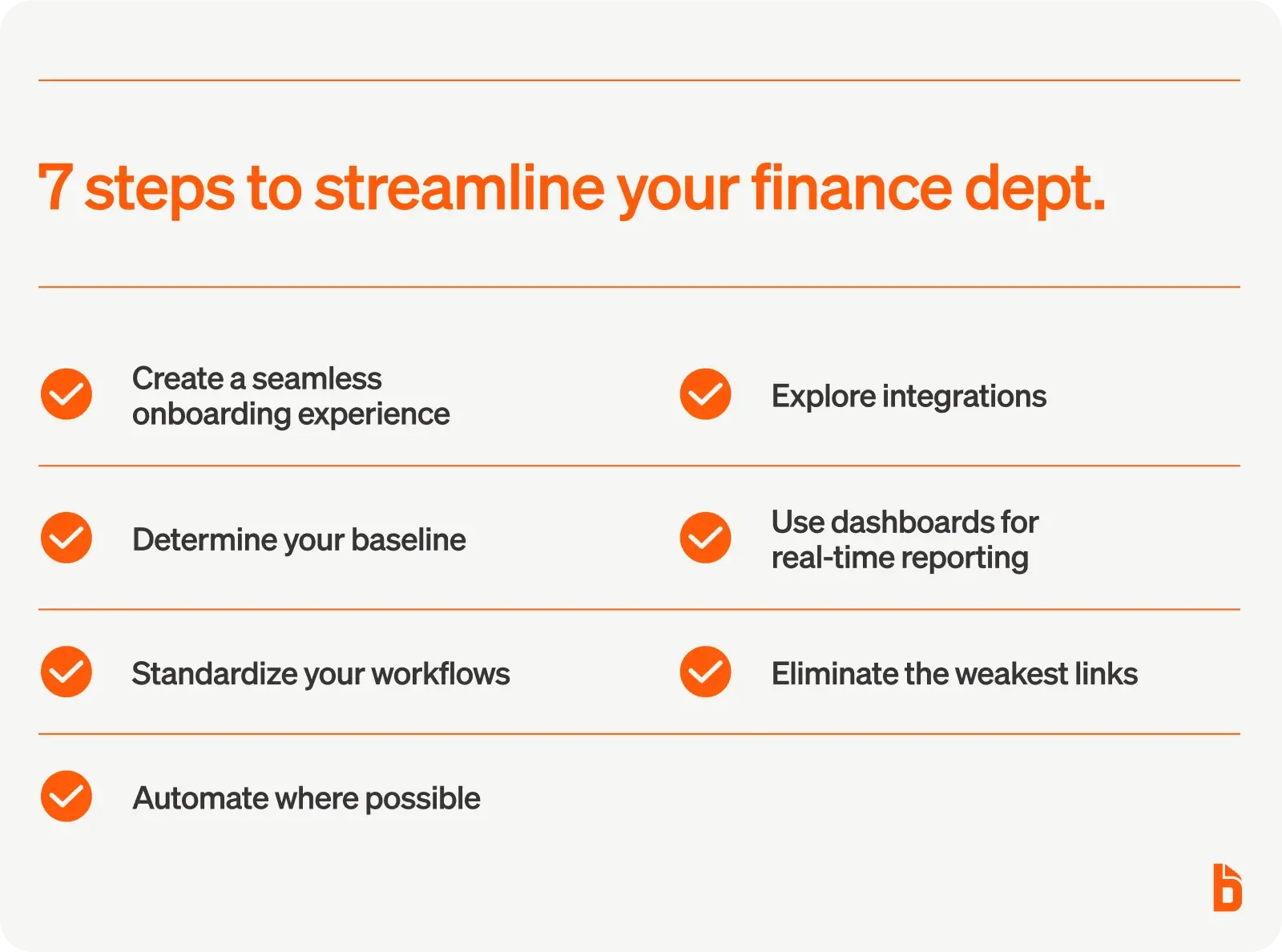

Steps to streamline your finance department

Ready to bolster the performance of your finance department? Take these seven steps to streamline their workflows and enjoy the benefits.

1. Create a seamless onboarding experience for new finance hires

Whether new hires are recent college graduates or veteran finance professionals, an onboarding plan helps ease the transition and reduce stress for other employees. Good plans typically include the following:

- Individualized welcome messages from the company and supervisors

- A clear outline of roles and responsibilities within the finance department

- A plan for their first 30, 60, and 90 days

- Straightforward processes for sharing and collecting paperwork

- Technology and software orientations

- “Cheat sheets” with new hire–specific FAQs

A thoughtful onboarding plan developed well in advance of a new hire’s first days can make the difference between an engaged finance team and a high turnover rate. Onboarding also gives you a chance to identify potential problems early and proactively address them.

2. Determine your baseline

Before making any changes, it is important to establish where your finance department currently stands. This involves analyzing how many invoices are processed per month, how many hours are spent on payroll, and how work is divided among employees. Keep in mind that workloads may vary depending on financial reporting schedules and other factors. To get the most accurate picture of average outputs, review at least a year’s worth of activities.

The figures pulled from an output analysis can be used to guide planning and growth projections. Depending on a company’s goals, these figures may help determine whether additional staff are needed to manage increased activity. The data can also be used as a benchmark for measuring future performance.

3. Standardize your workflows

Relying on ad hoc reporting practices means the finance department needs to spend additional time defining the work to be done before they start with the reporting. With standardized workflows, everyone knows exactly what needs to be done and how to do it.

Once you have standardized workflows in place, you’re able to identify the choke points that need the most amount of optimization and refinement. Go through the process step-by-step with the team and get feedback on what aspects can be improved.

4. Automate whenever possible

Automation capabilities have advanced substantially in the past decade, and that is good news—shifting from manual to automated processes saves time and allows employees to focus on more strategic tasks that drive faster growth and enable higher-quality services.

For example, accounts payable (AP) automation seamlessly enforces workflows to ensure bills are digitally reviewed, approved, and paid. Now is the time to upgrade your finance department with automated programs to keep up with a rapidly changing world.

5. Explore integrations to reduce duplicated efforts

Connecting software within your financial stack allows information to flow freely through your financial systems in real time and eliminates the need to manually enter the same data twice. Linking accounting systems or enterprise resource planning (ERP) programs with payroll and AP systems, for instance, can save hours each month. This makes it easy to track each step of your financial processes and avoid duplicate payments, overpayments, or other errors.

Start by reviewing your finance department’s current processes to identify where manual steps are still being used. From there, research solutions that automate these processes and integrate with your existing systems to lighten the lift. It takes time to find and implement the right solutions, but this initial investment will pay off in the long run.

6. Use dashboards for real-time reporting

With integrations and automation set up, you have the opportunity to create dashboards that update with the latest data, all without lifting a finger. Dashboards are where you can elevate the most essential information, saving everyone from digging for the information they need.

Some examples of how you can use dashboards include:

- Monitoring budgets vs actuals

- Track recent transactions on company cards

- Get a pulse on progress towards key performance indicators (KPIs)

- Identify upcoming due dates for accounts payables and receivables

- Prompt alerts from potential fraudulent activity

- Find potential cash flow issues before they happen

7. Eliminate the weakest links

While automation and integration can eliminate most inefficiencies, it is worth digging deeper to root out any lingering weak links and bottlenecks. One approach is to have employees calculate the amount of time they spend on their daily activities, establish reasonable time quotas for each activity, and then brainstorm ways to stick to them. Keep in mind that even easy wins are worth celebrating since a few minutes each day adds up over time.

Optimize your finance functions with BILL

Optimizing finance functions is an ongoing project—reviewing outputs and automation software solutions at least once a year can keep your company’s wheels turning smoothly while ensuring employees remain happy. The seven steps above can set the process in motion and streamline your finance department for increased efficiency.

And when you’re ready to start automating, BILL can help. With tools that automate accounts payable, accounts receivable, cash flow forecasting, and more, your team will save time and get to focus on the high impact work that matters.