Whether you’re making a payment or getting paid, routing numbers help direct your funds from one account to another. This article covers what routing numbers are, why they matter, how to find and read them, and how they work with account numbers to get your money to the right place.

What is a routing number?

A routing number is a nine-digit sequence of numbers that can help identify financial institutions in the United States.

A large bank might have multiple routing numbers that map to different states, regions, or branches, but each routing number only maps to one banking institution.

How does a routing number work?

Routing numbers identify the origin or destination of payments through the nine-digit sequence of numbers.

When a check is deposited, the bank uses the routing number to identify where the payment is coming from. It can then process the request to “pull” the funds from its origin and deposit them into the receiver’s bank account.

In the case of electronic payments, it’s common for routing numbers to be provided to the payee. The payee provides the routing number to the payment method as the destination of the funds. The payment method pulls the funds from the bank account (or other funding source) and then “pushes” them to the destination, as identified in the routing number.

Think of routing numbers like addresses that are used in pick-ups or deliveries. When provided, your bank knows exactly where to go to “pick up” the funds, or where to go to “deliver” the funds and complete the payment.

Is an ABA number the same as a routing number?

Yes, an ABA number is the same as a routing number. The term “ABA” stands for American Bankers Association, the organization that first established routing numbers more than 100 years ago.

ABA routing numbers are granted to financial institutions that are recognized by the ABA, the Federal Reserve, and other federal or state charters.

Is a transit number the same as a routing number?

In the US, generally speaking, a transit number is the same as a routing number. In fact, transit numbers or routing numbers are sometimes called “routing transit numbers.” They’re all the same thing.

That said, there are two things to be aware of:

- Canada banks use numbers called “transit numbers” that are only 5 digits. They accomplish the same thing, but they work a bit differently than banking numbers in the US.

- Don’t confuse a transit number with a wire transfer number, which may also be called a wire transfer routing number.

Is a SWIFT code the same as a routing number?

No, they are not the same. Bank routing numbers are used in the US for domestic payments. A SWIFT code is used for international payments. SWIFT stands for Society for Worldwide Interbank Financial Telecommunications.

What is a routing number used for?

Routing numbers were originally designed to ensure that paper checks were sent (or “routed”) to the right financial institutions. Today, routing numbers have become an important tool in all types of banking activities, for both traditional to electronic transactions.

Here are a few examples of what routing numbers are used for:

- Connecting your bank account to a payment app

- Opening a new brokerage account

- Direct deposit information for your paycheck

- Establishing auto-draft for monthly bill payments

- Connecting your account to your accounting software

- Opening a new online store

- Enabling electronic transfer payments for utility bills

- Setting up your business website to accept direct deposit payments

- Ordering new checks

- Paying taxes online via bank draft

- Requesting a tax refund electronically

- Setting up an electronic funds transfer

What do routing numbers mean?

Because routing numbers were established more than a century ago, the first four digits of a routing number used to represent the physical location of a bank.

Today, however, banks move fairly often. A bank might also acquire or merge with another bank, transferring those routing numbers to the new institution. So routing numbers are less tied to physical locations than they once were.

Nonetheless, when a new bank is formed, it will still get a routing number associated with the closest Federal Reserve Bank.

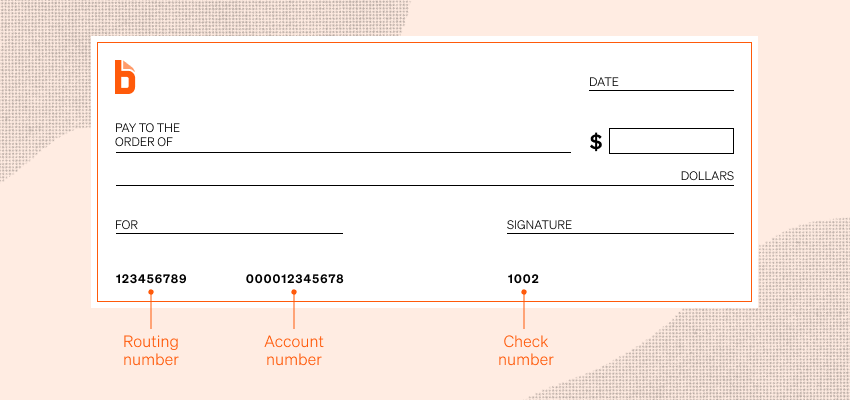

Example of a routing number

How many digits is a routing number?

A routing number is 9 digits. That’s a billion possible numbers, making sure each routing number is unique and maps to only one US financial institution.

The first two digits of a routing number represent which Federal Reserve bank is responsible for routing a check or other transaction, while the third digit represents which processing center in the Federal Reserve processes the transaction. The fourth digit represents the Federal Reserve district where the bank is located. The next four digits identify the specific bank.

Finally, the ninth digit is generated by a checksum equation involving the first eight digits and is used as added security for transactions. If the result of plugging the first eight digits into the equation isn't a final sum equaling the ninth digit, then the transaction is processed manually for security purposes.

Where is the routing number on a check?

Generally speaking, the routing number is the first number listed at the bottom left corner of your checks. This is followed by your account number at the bank and then the number of the check.

Machine-readable symbols usually separate each of these numbers, making them easy to distinguish from each other.

How to read the routing number on a check

To read the routing number on a check, simply find the nine-digit number at the bottom. It will usually be the first number in a list of numbers.

That said, if the first number in the list is not nine digits, that’s not the routing number. The routing number should be nine digits long. You can also look in your banking app or visit your bank’s website to confirm your routing number.

How to find your routing number

Here are several options for how to find your routing number:

- Paper check. Your routing number is located on the bottom left of your paper checks. It should be the first nine-digit number in a list of numbers. In some kinds of checks, the routing number might not be first, so make sure the number has nine digits.

- Bank website. You can usually find your routing number on your bank’s website. It might be in the footer, in the help center, in your account information, or somewhere else. Still, if you’re willing to look around a bit, you can usually find it without too much trouble.

- Bank statement. Many banks include your routing number on your monthly statements. Browse through the information that’s included at both the top and bottom of each statement. If it’s a printed statement, it might even be on the back.

- Mobile app. Your bank’s mobile app probably includes your routing number. Because every app is unique, you might have to hunt around a bit.

- ABA routing number search. Some banks include a lookup service for their own routing numbers, and the ABA offers this option too. However, you should use this system with caution. If you opened an account in a different state and then moved—or even if your branch moved—the original routing number may follow your account, so you can’t always rely on a location-based lookup service.

- Call your bank. If you’re really stuck and you can’t find your routing number, call your bank. They should be able to look up your specific account and locate your routing number for you.

Routing number vs. bank account number: what's the difference?

Routing and account numbers are used for different steps in processing money transfers.

Your routing number indicates which Federal Reserve Bank should process your transactions, and it identifies your banking institution. It uniquely identifies your bank.

If you found a random slip of paper with just a routing number on it, you would be able to identify a specific bank from that number, but not a specific account.

Your account number, on the other hand, is the number of your specific bank account at that bank. It uniquely identifies your account, but it doesn’t include any information about where that account is.

If you found a piece of paper with an account number but no routing number, you would have no idea what bank that account belonged to.

That’s why you need both pieces of information to fully identify a bank account—the routing number and the bank account number. If you only have the routing number, it could be any account at that bank. If you only have an account number, the account could be anywhere.

That said, remember that routing numbers are public information. If someone knows your account number and also knows (or could guess) which bank you use, they can always look up the routing number. That’s why it’s so important to keep your bank account number private, just like your Social Security number or your debit card’s PIN code.

How to send money with an account and routing number using BILL

BILL is a business-to-business (B2B) payments service that lets you make and accept payments electronically. When you invite your vendors to manage their own account in the BILL network, neither of you needs to see the other’s account information.

You can connect to BILL with your routing number and account number, and they connect to BILL with their own information. Once you’re each connected, you can send and receive ACH payments and more.

You can also send payments to businesses that choose not to connect to BILL, including ACH payments, credit card payments (even if they don’t take credit cards), international wire transfers, and paper checks that BILL will print and mail for you.

To see how it works, watch a demo or sign up for a risk-free trial. There's no credit card required to give it a try.

Frequently asked questions

What is the difference between a routing number and an IBAN?

An IBAN (or international bank account number) is a code used to identify bank accounts internationally. They are composed of 34 characters, both letters and numbers, to identify the bank, country, and account number of the recipient of a cross-border payment.

When sending and receiving payments domestically, you only need to know the routing number, as the routing number identifies the bank or institution. But international payments will require knowing the IBAN.

To find your IBAN, check your bank statement, use an IBAN calculator, or request it directly from your bank.

Is it possible to have two routing numbers?

Yes, some banks will have two routing numbers. A common reason for this is having unique routing numbers for different payment methods, like low-value ACH payments and high-value wire transfers. Additionally, large institutions may have multiple routing numbers for different states, regions, or branches.

Does the account number or routing number come first?

On a check, the routing number appears first, followed by the account number. This is so the bank processing the payment knows the institution to send the money to, before narrowing it down to your specific account details.

Can routing numbers change?

Yes, routing numbers can change. This would only happen in the instance of a bank merger, acquisition, branch closure, or restructuring.

Do online banks have routing numbers?

Yes, all banks, including online-only or digital banks, have routing numbers for sending and receiving money. If you do not have a check that you can access a routing number from, look in your online account or request it from the online bank.

Are routing numbers always nine digits?

In the United States, routing numbers are always a nine digit code. If a routing number doesn’t have nine digits, it’s likely an international bank account. For example, Canadian bank accounts have eight-digit routing numbers comprised of a five-digit transit number and three-digit institution number.